AI-Durations™

AI-Convexities™

Transparent TBA Analytics

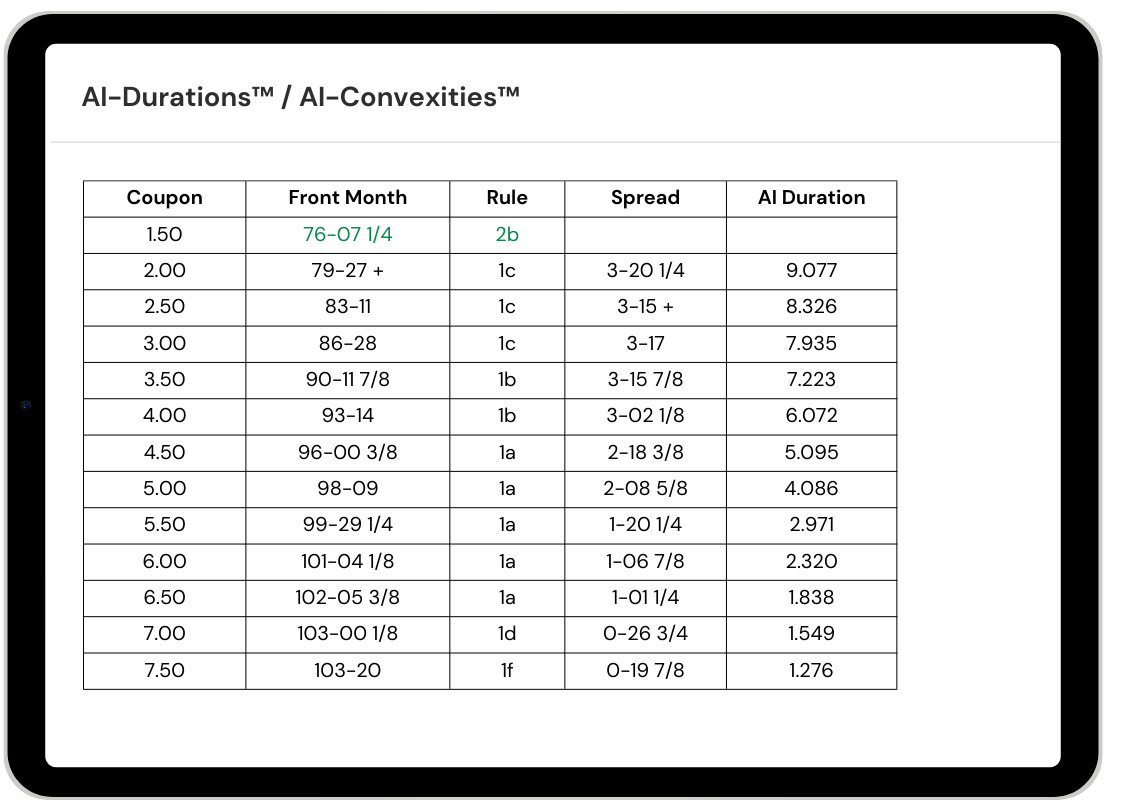

A simplified and transparent methodology used to derive TBA Durations and Convexities, utilized by the CME for InterCommodity Spreads (ICS).

TBA Futures – CME Group

MIAC’s AI-Durations and AI-Convexities are derived from MIAC TBA Fixings. The actual market price fixing of each adjacent TBA Coupon is used to derive the Implied price sensitivity of each TBA Coupon. However, because of the underlying price volatility and variability embedded in the TBA market, a time series of implied price sensitivities is used to derive the average implied (AI) Durations and Convexities.

MIAC uses a Constant OAS methodology integrated with CORE™ voluntary and involuntary behavioral models to derive fair value payups relative to benchmark TBA levels. These values are incorporated directly into MarketShield pricing and hedge analytics.

MIAC Market Monitor empowers originators and investors with reliable price discovery, enhancing their decision-making process in the dynamic TBA Market.