MIMs™

Mortgage Industry Medians

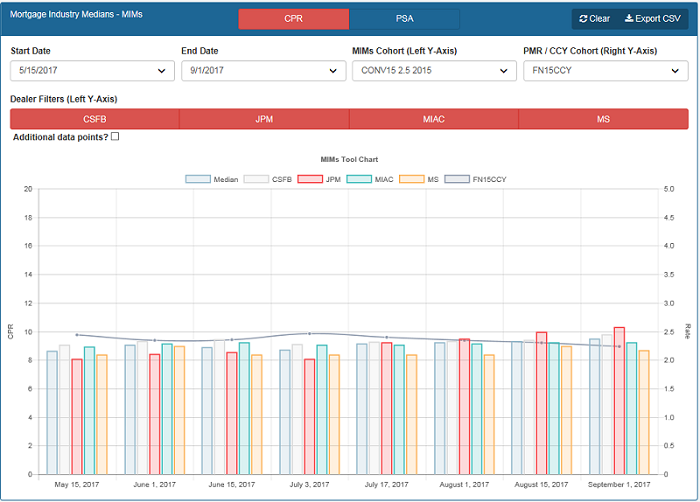

Mortgage Industry Medians (MIMs) is a semi-monthly dealer consensus of long-term prepayment projections. The MIMs survey is based on MIAC’s Generic Cohorts, which are derived from broad-market MBS data and differentiated by product type, coupon, and issue year.