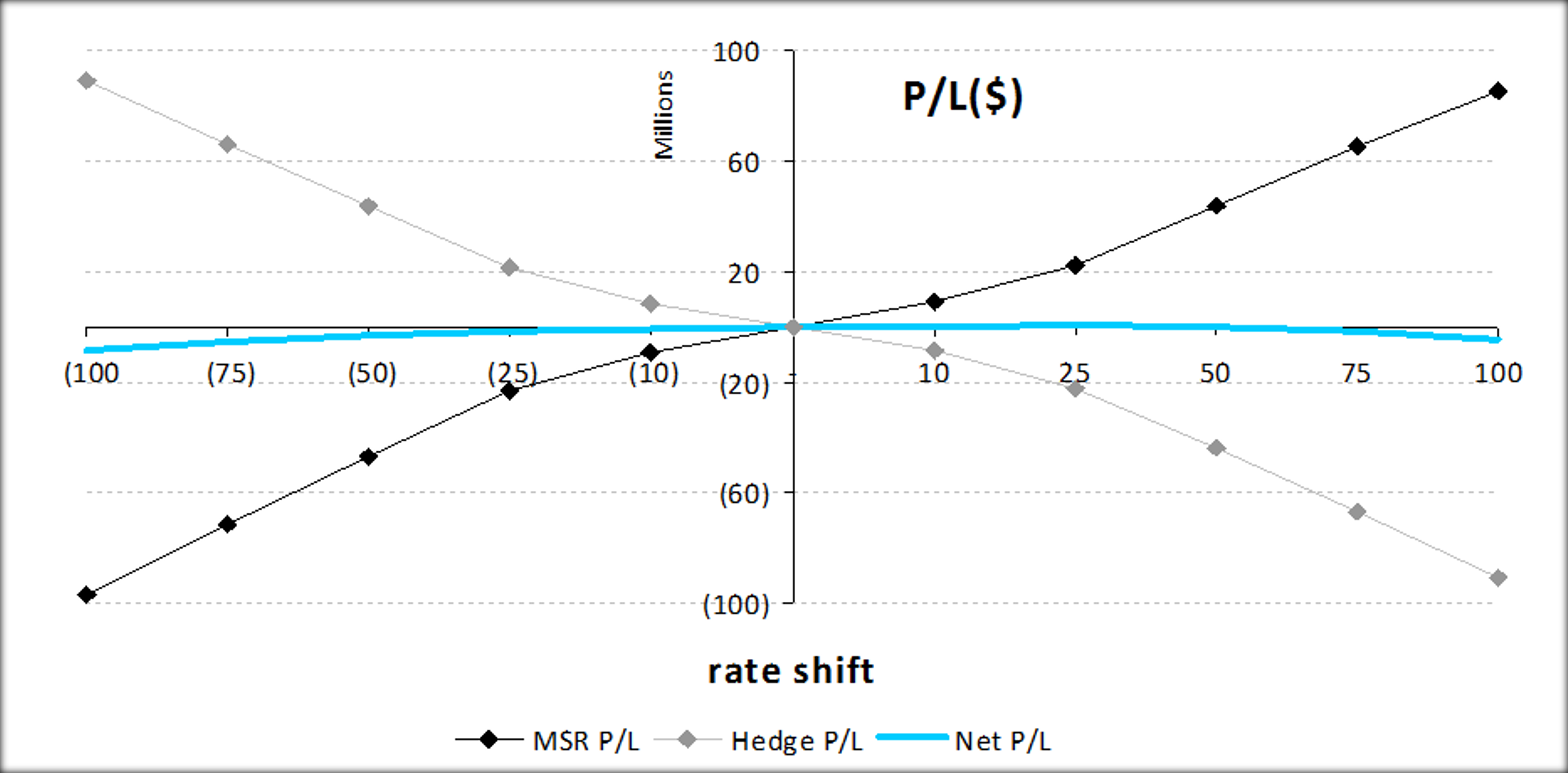

MSR Hedge Advisory

In addition to our MSR valuation capabilities, MIAC offers MSR hedge advisory services. Our advanced term structure model, comprehensive risk metrics, rigorous and robust protocols, and large hedge instrument library enables our team to synchronize with the business objectives of our clients.