Additional Features

CORE™ model projections incorporate both home prices and unemployment change. We track detailed loan status from Current through REO, including time spent in each state. Granular sub-models capture distinct behavior within sectors and products, supporting predictive delinquency and foreclosure forecasts.

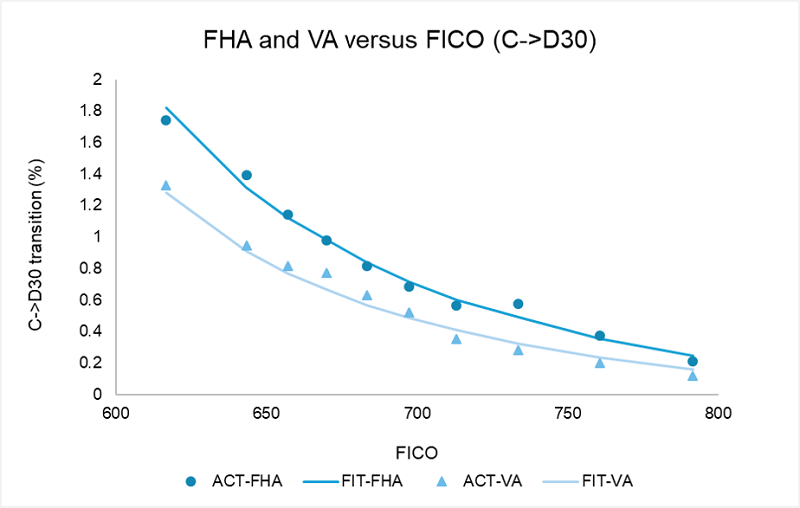

- Within GNMA: FHA loans have worse credit than VA after adjusting for attributes

- Within Non-QM: DSCR, Bank Statement and Full Doc

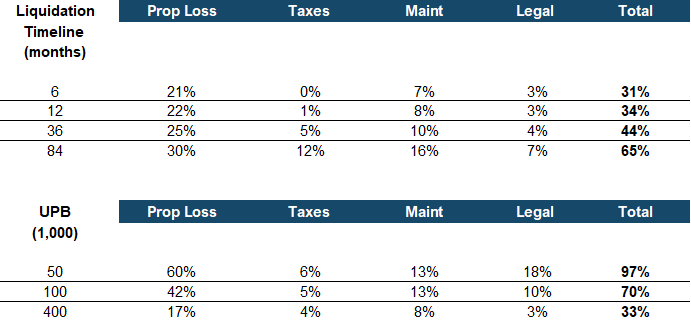

- Probability-of-sale (POS) and judicial foreclosure (FCL) timelines

This statistical framework allows for complex and non-linear behavioral responses, to support the handling of competing risks.