VAST™

Variable Assumptions Set Tool

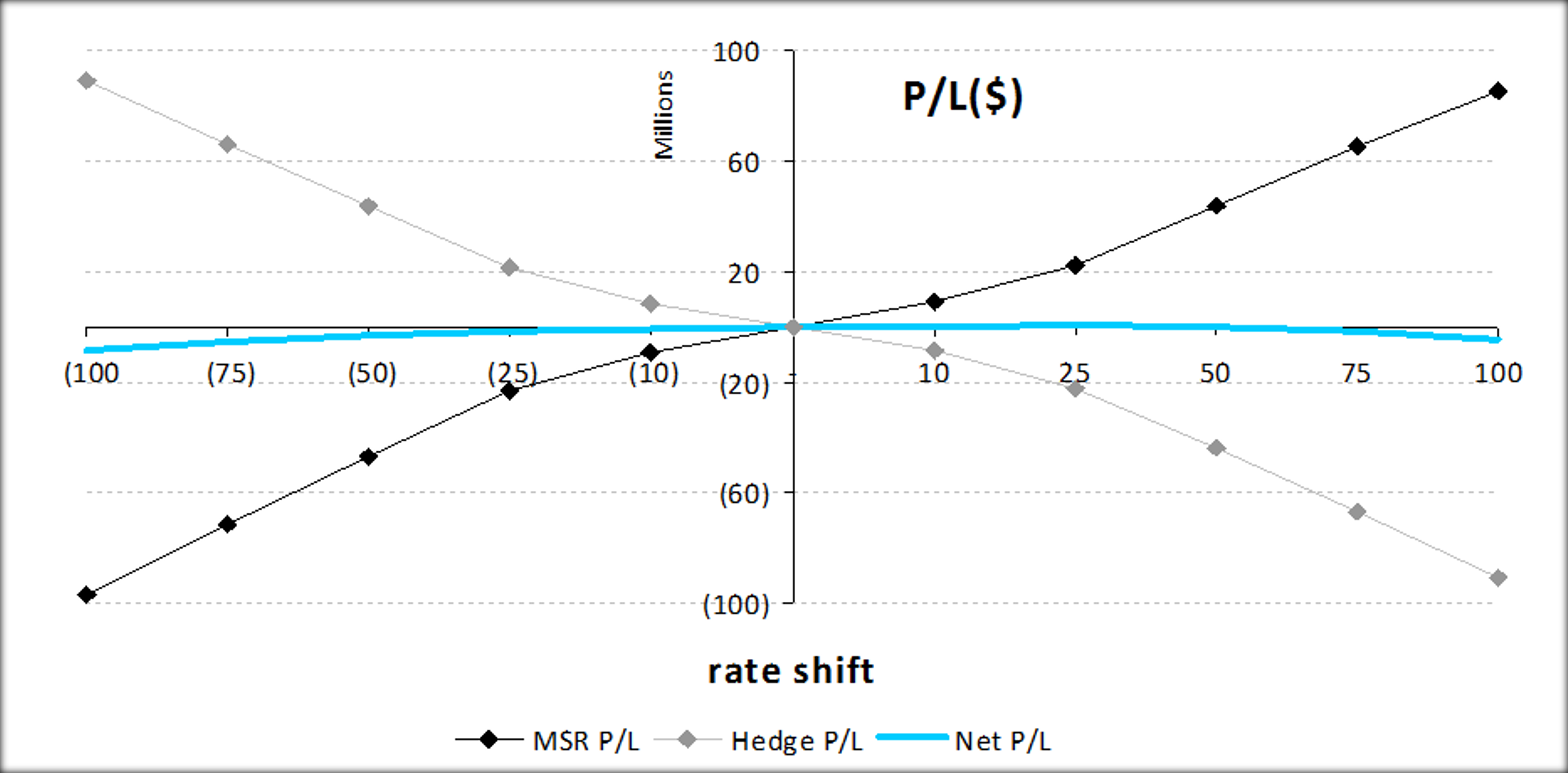

VAST™ evaluates the price performance of the MSR, Whole Loan, and associated Hedge Instruments, both prospectively and through retrospective analysis.

VAST™ is a mortgage risk analytical software model for mortgage asset classes in both residential and commercial sectors, and a family of long-dated interest rate derivatives.

VAST™ enhances understanding of both prospective and retrospective market value risk and allows users to control model parameters including term structure shape, basis spreads, forward time periods, volatility surfaces, prepayment models, foreclosure, and loss simulation.

We closely work with the client’s IT department for software installation. We create and provide the initial setups based on the client’s specifications. This saves the client FTO hours so they can focus on training.

We offer 2+ days onsite training and often follow-up with online sessions to reinforce training material. Our web-based support ticketing system allows clients to easily submit requests and monitor its progress. Our support team members work from several locations, which means we offer longer working hours.

We pride ourselves on hiring talented and experienced employees. We are staffed with industry experts who have worked in many facets of the financial sector for decades, making it easy for us to relate to the needs of our clients.