This is the second edition of Research Insights, taking a closer look at liquidation timelines. Because this is a complex subject, this edition focuses on a few key themes. Additional details will be addressed in future editions of our Research Insights series.

What are Liquidation Timelines?

We define the liquidation timeline for a residential loan to be the number of months it takes to resolve a distressed asset, from initial delinquency through final resolution. In order to operationalize this concept, several conventions need to be adopted. For example, a loan may become seriously delinquent (hereafter, SDQ), cure back to current, become seriously delinquent a second time, and then finally resolve with a loss. This SDQ->Cure->SDQ cycle can occur repeatedly. The analyst needs to decide if the timeline should be measured from the first serious delinquency, the last, or some mixture of the two.

A second complication is that a loan can liquidate with a loss via many paths, such as completion of a foreclosure and REO sale, a borrower-titled short sale, or a third-party take-out. Short sales are very common in all residential sectors, so any measure of liquidation time needs to extend beyond just “time in foreclosure”.

We adopt a simple measure of liquidation timelines: Conditional on a loan liquidation, we record the number of months past due as of that liquidation date. This definition is both simple to apply to actual data, and fully consistent with our Core Residential Valuation Model. This realization-based measure (i.e., where we only sample fully resolved assets) avoids the censoring problems that can exist with other metrics.

Why Should Market Participants Care About Liquidation Timelines?

Liquidation timelines have a significant impact on loss severities. In turn, loss severities have a large impact on whole loan valuations, risk sensitivities (such as duration and WAL), and stress valuations. Loss severities are even important for loans with credit enhancement, such as private mortgage insurance or a VA guarantee, since there is usually some probability that the insurance or guarantee will not fully cover the actual loss. Liquidation timelines also play a vital role in an MSR context, for both valuations as well as advancing/cash flow analysis. The impact of liquidation timelines on MSRs will be addressed in a forthcoming Research Insights.

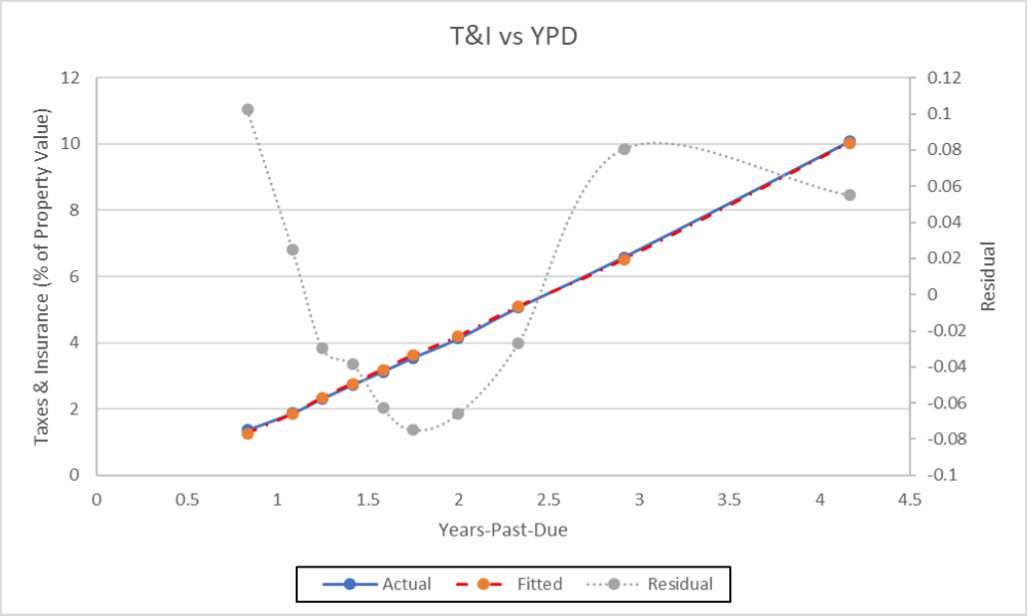

Figures 1-3 highlight the impact of timelines on various components of loss severity. Figure 1 shows the relationship between escrow (i.e., Tax and Insurance) expenses and the realized liquidation timeline. We represent timelines in terms of years past due rather than months past so that readers can interpret these data in annualized terms. The actual liquidation can be the sale of an REO property (where title is obtained via a completed foreclosure), the receipt of proceeds from a borrower-titled short sale, or any other foreclosure alternative.

Expenses are shown as a percentage of the estimated property value as of the dated date of the last paid installment. The underlying data is obtained from the FHLMC Loan Level Dataset. The predicted value of the Tax and Insurance loss component is obtained from the Core Residential Valuation Model. As is evident, escrow expenses increase linearly as a function of the realized liquidation timelines. States with higher average taxes or insurance costs will of course have a higher slope, and this is captured by our Model. A complete description of our Core Residential Valuation Model, which includes the Loss Severity sub-model, is available from your MIAC sales coverage.

Figure 2 is analogous to Figure 1, except that it displays maintenance expense (again, as a percentage of estimated property value) versus the realized liquidation timeline. The same pattern is evident, although there is a very mild quadratic effect at large values of years past due. Maintenance costs vary quite a bit across states, and this is also captured by our Model.

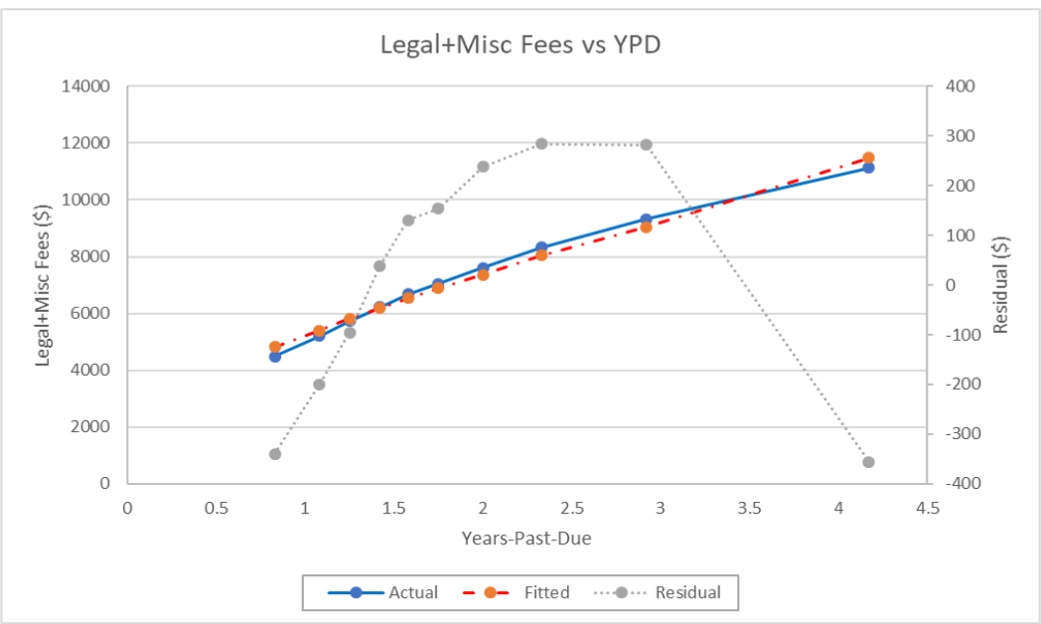

Finally, Figure 3 displays legal and miscellaneous costs (in $ terms, rather than as a % of estimated property value) versus realized timelines. Once again, we see the same pronounced effect of liquidation timeline on this important component of loss.

In contrast to the above three loss components relating to expenses, net proceeds from property liquidation (another significant driver of losses) has a very limited dependence on realized timelines after controlling for other variables such as mark-to-market LTV, UPB, occupancy and loan purpose.

It is well established that loss severities have increased substantially since the housing crisis. See, for example, the Federal Reserve Bank of Philadelphia Working Paper 17-08 entitled “Regime Shift and the Post-Crisis World of Mortgage Loss Severities”}. Figure 4 shows that this increase is due, in large part, to average liquidation timelines rising over this period, in fact, more than doubling between 2008 and 2016.

The Mechanics of Timelines in MIAC’s Core Residential Valuation Model

Our Core Residential Valuation Model was completely revamped in early 2019. This new model fully integrates the transition and loss severity sub-models. In order to explain what we mean by fully integrated some background is needed.

The responsibility of the transition model is to predict the probability that a given loan is in all feasible delinquency statuses at every month in the future. For example, consider a loan that starts out as current. The transition model will predict the probability that the loan remains current, transitions to D30, or prepays at the end of the month. At a horizon of 12 months, many more states are of course feasible, and our model computes the probability of all feasible states.

In any transition model, liquidation and prepayment are terminal (or absorbing) states. In other words, once a loan transitions to either loss liquidation or prepayment, it becomes and remains inactive. In contrast, serious delinquency (SDQ), foreclosure, and even REO are active states. For example, consider a loan that starts out as D120. That loan can cure to a less delinquent state, remain in serious delinquency, transitions to FCL, or liquidate via borrower-assisted short sale.

Within our model framework, we define the liquidation timeline as the expected months past due (equivalently, the cumulative number of missed payments) conditional on the loan having liquidated, at each projection month. Importantly, liquidation timelines are an outcome of our transition model framework. In other words, they are fully implied by our transition model specification, and no additional assumptions are needed.

To see this, consider a simplified framework where loans can only liquidate from a completed FCL and subsequent REO liquidation. In that case, the average liquidation timeline will be driven entirely by transition rate of SDQ to FCL (SDQ->FCL), the transition rate of FCL to REO (FCL->REO), and finally the transition rate of REO->LIQ. Any loan attribute or macro-factor which reduces those transitions will lengthen the average amount of time the loan spends in each state, and thus increase average liquidation timelines. In the more complex structure underlying the Core Residential Valuation Model, average liquidation timelines will also depend on the resolution mix predicted by the model, as we discuss below.

As indicated previously, the severity model and the transition frequency model are fully integrated. This means that the timelines predicted by the transition model are input into our loss severity model. In other words, the responsibility of the transition model is to produce expected timelines at every projection month, and the responsibility of the severity model is to consume those timelines and produce an expected loss.

The Evolution of Projected Liquidation Timelines in Core Residential Valuation Model

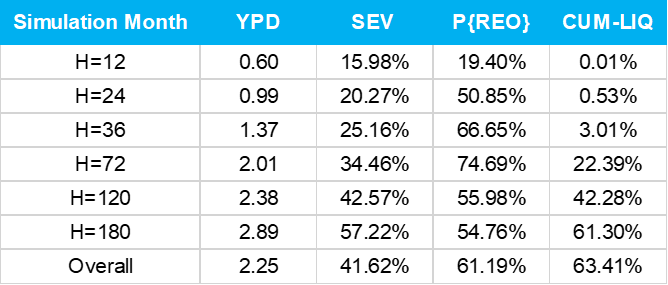

In order to highlight these ideas and explore some additional consequences of our Core Residential Valuation Model, we ran a hypothetical newly originated Agency loan with the following characteristics: $250k balance, 750 FICO, 75% LTV/CLTV. We decided to run a “synthetic average” Judicial state. By synthetic average, we mean that this is representative of Judicial states overall, and not of any single Judicial state in particular. We use this for our production runs on portfolios that are reasonably representative of Judicial states overall. As is well known, there is considerable heterogeneity within the Judicial/Power of Sale (POS) segmentation. It is perhaps less well known that there is segment overlap: the slowest POS states are slower than the fastest Judicial states. In a forthcoming Research Insights, we’ll delve into this topic in more detail.

The results of this analysis are displayed in Figure 5. The most significant observation is that expected timelines continuously increase over time (i.e., as the loan seasons). This is partly the result of the REO/Short-sale mix changing across projection months. Conditional on a loan liquidating early on, there is a higher probability that it was short sale resolution. However, timelines would also increase over time if short-sales did not exist and all liquidations were the result of foreclosure/REO resolutions.

Primarily because of the increase in expected timelines, expected severities will increase over time as well. Consequently, it would be highly imprudent to “guestimate” a deal’s long-term severity by looking at severities observed over the first few years. As the above discussion makes clear, those are likely to be the lower severities that the deal will ever experience.

Figure 1 Source: MIAC Analytics™

Figure 2 Source: MIAC Analytics™

Figure 3 Source: MIAC Analytics™

Figure 4 Source: MIAC Analytics™

Figure 5 Source: MIAC Analytics™

Author

Dick Kazarian, Managing Director, Borrower Analytics Group

Dick.Kazarian@miacanalytics.com

"*" indicates required fields