BondAgent™

Structured Products Software Solution

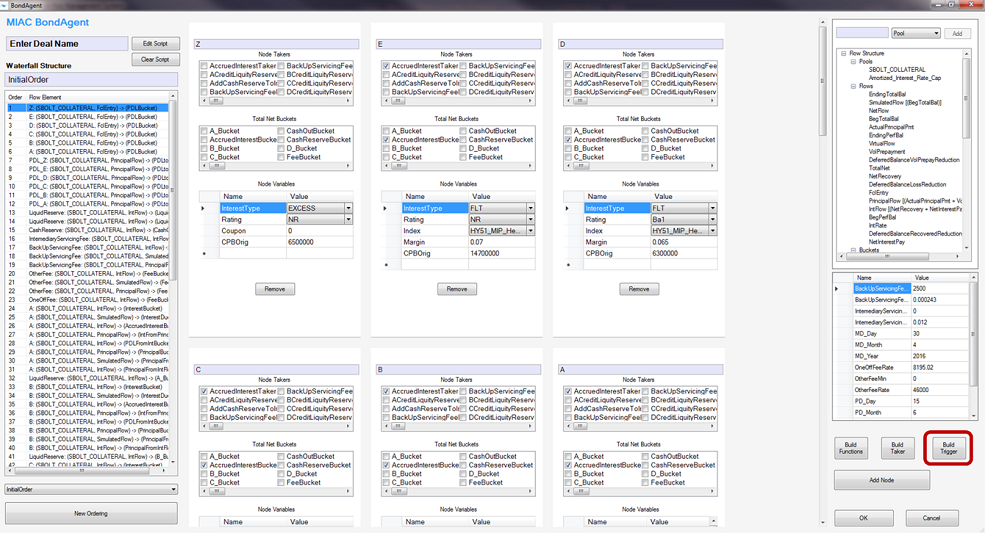

BondAgent™ is designed to create waterfall cash flows and bond analytics from collateral data. Built into Vision™, and leverages MIAC CORE™ – macro-factor driven, loan-level credit, and prepay models.

Advanced cash flow risk analytics are integrated into BondAgent™.

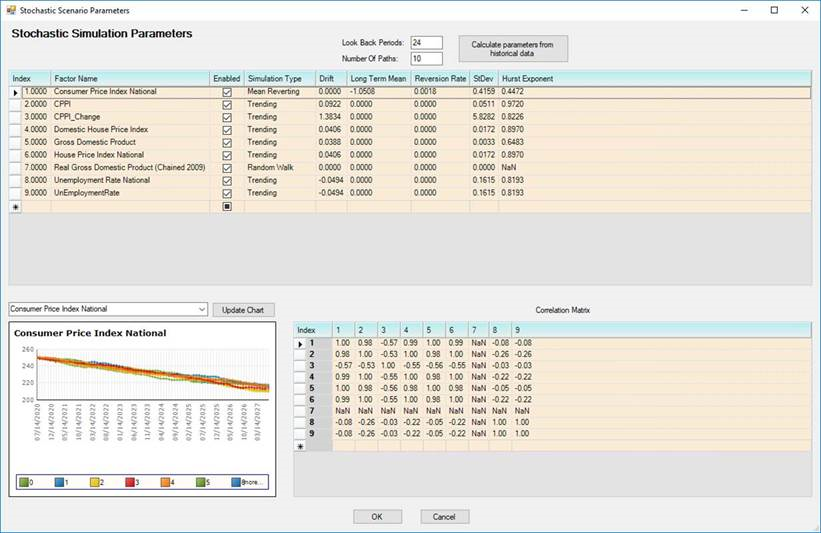

BondAgent performs stochastic analysis of collateral model drivers for cash flow generation.

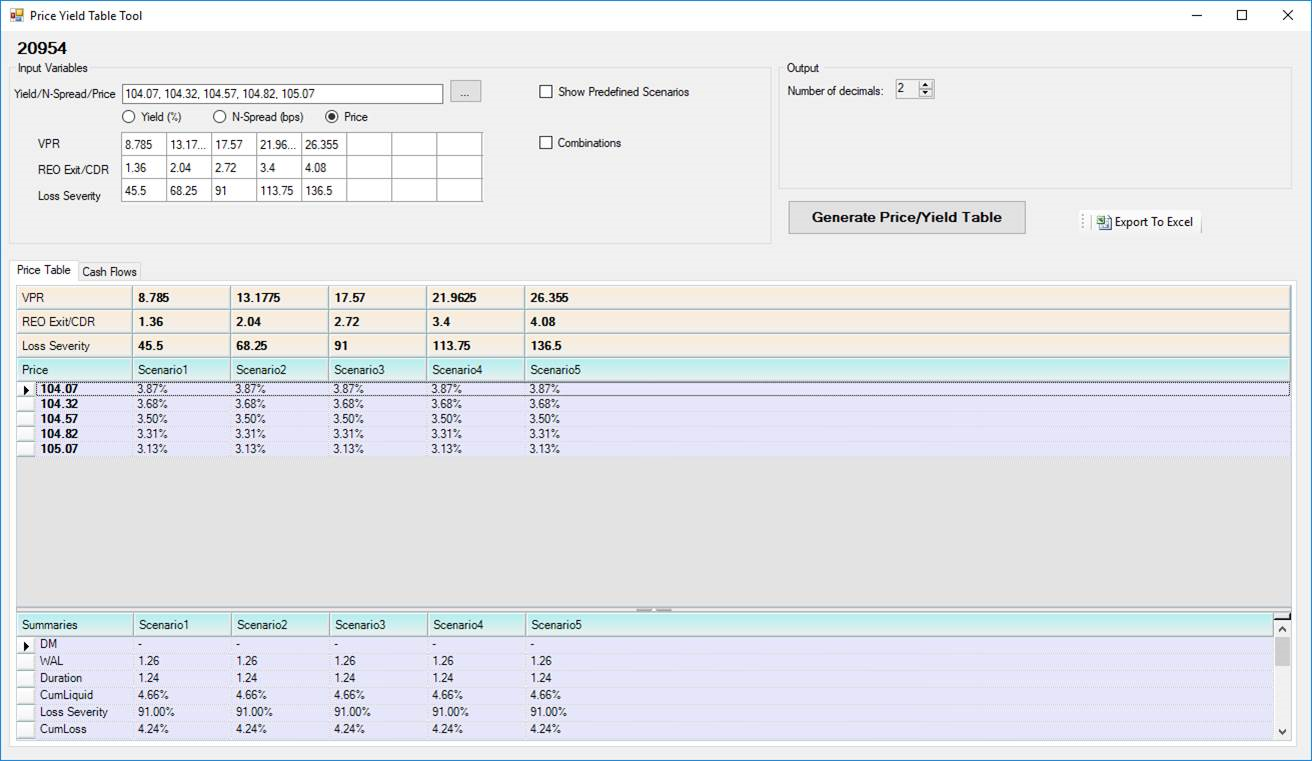

Update collateral and bond pricing assumptions.

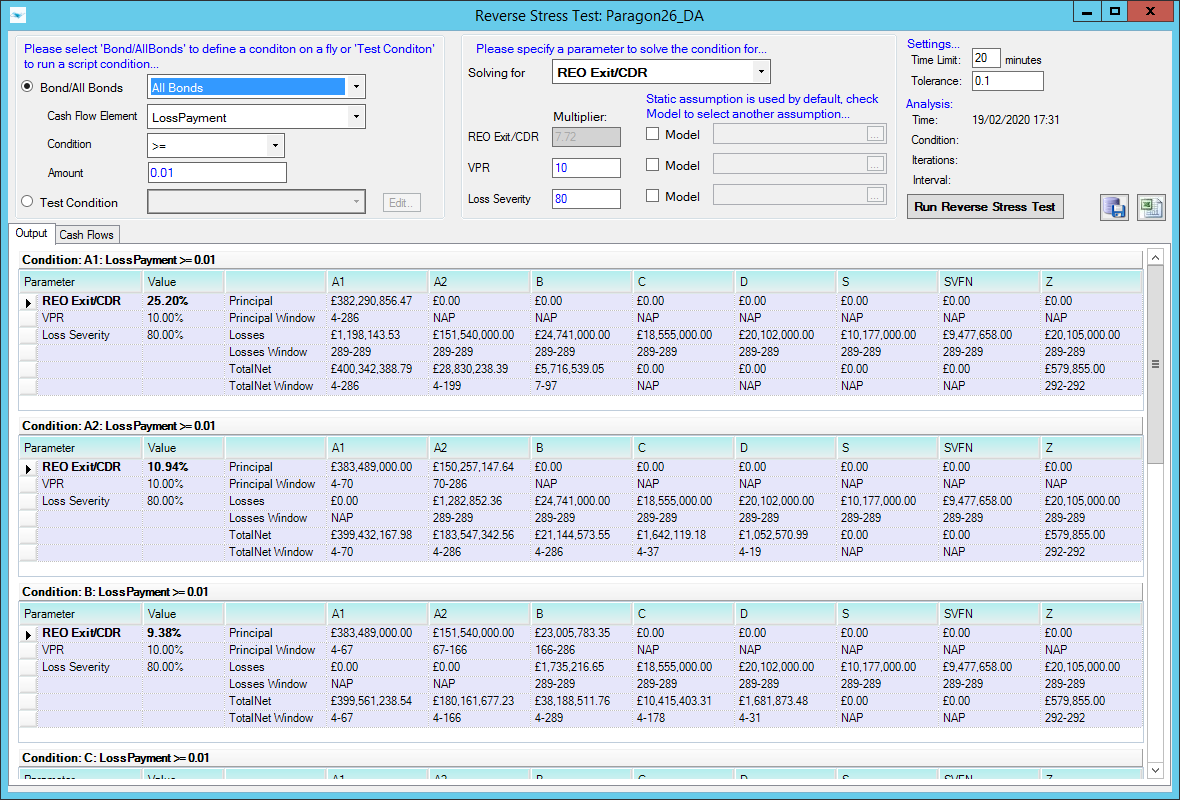

Reverse Stress Testing determines the specific levels of CDR (or REO Entry) Pct, CPR, or Loss that result in user-defined levels or loss or paydown for the bond.

MIAC utilizes BondAgent™ to generate Risk Retention analysis, bond price discovery, and investor reports for structured finance products for our clients.

We closely work with the client’s IT department for software installation. We create and provide the initial setups based on the client’s specifications. This saves the client FTO hours so they can focus on training.

We offer 2+ days onsite training and often follow-up with online sessions to reinforce training material. Our web-based support ticketing system allows clients to easily submit requests and monitor its progress. Our support team members work from several locations, which means we offer longer working hours.

We pride ourselves on hiring talented and experienced employees. We are staffed with industry experts who have worked in many facets of the financial sector for decades, making it easy for us to relate to the needs of our clients.