By Mike Carnes, Managing Director, MSR Valuations Group

MSR Price Changes (YTD 2022)

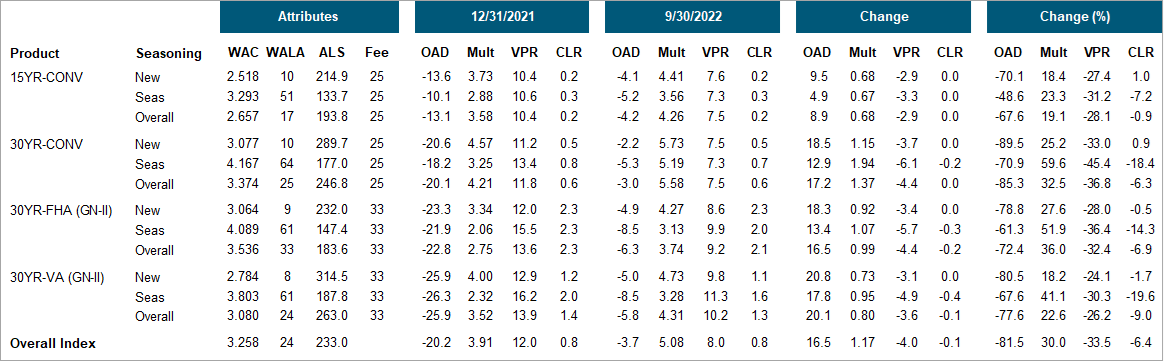

As displayed in Figure 1, MIAC Generic Servicing Assets™ (GSAs) have experienced significant YTD 2022 price increases across all four sectors and both vintages, with a UPB-weighted increase of 1.17 multiple (or 30.0%).

Within Conventional products, pricing increased substantially more for 30-year than for 15-year, in both absolute (1.37 vs. 0.68 multiple), as well as relative (32.5 vs. 19.1%) magnitude. This is primarily due to the less negative 15-year option-adjusted durations (OADs) at the start of 2022 vs the substantially more negative 30-year OADs (-13.1 vs. -20.1). In contrast to Q1 2022, the cumulative sell-off in 30-year primary rates (PMR-30) over the first three quarters was nearly identical to the PMR-15 sell-off.

Looking across the 30-year sectors, Conventionals had the largest absolute price increase, followed by FHA and finally VA. But FHA multiples are generally lower than Conventional and VA multiples, so their percentage price increase was the largest (at 36%). Also note that, for each sector, the seasoned vintages experienced greater price increases than the newly issued vintages (defined as pool age less than 24 months). This is because the seasoned vintages have much higher WACs (by 70-100 bps), and so benefitted much more from the rate sell-off. In other words, loans that are closer to in-the-money (ITM) have greater rate sensitivity than loans that are already out-of-the-money (OTM). This is also evident from the much larger VPR drops on the seasoned vintages.

Figure 1: GSA Changes (YTD) Source: MIAC Analytics™

MSR Duration Changes (YTD 2022)

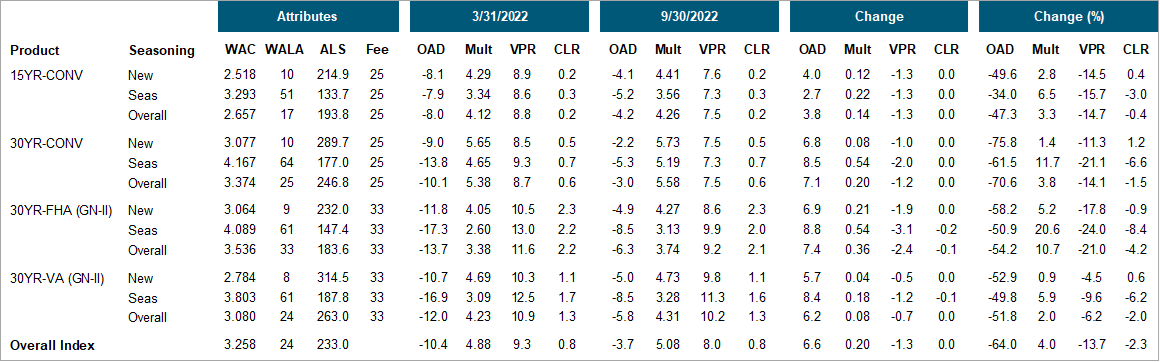

The option-adjusted duration (OAD) of the aggregate GSA universe became substantially less negative, moving from -20.2 to -3.73, over the 12-31-21 to 09-30-22 period. In fact, some GSA cohorts are now exhibiting durations close to zero. The OAD change was similar across the 30-year sectors and was much more muted for the 15-year Conventional mortgages. The OAD impact from the rate sell-off depends on numerous factors, the most important of which is the rate sensitivity of prepayments (i.e., the slope and curvature of the s-curve). As a result of these dramatic OAD changes, MSR owners who hedge their positions would have needed significant adjustments to their hedges to maintain their desired exposure to rates.

MIAC’s Hedge Advisory team provides highly customized hedge recommendations based on each client’s objectives, risk tolerance, and approved instruments. The sensitivity of OADs (and other risk sensitivities) to changes in collateral attributes and market conditions is one important reason that MSR Hedge Advisors need to have reliable analytics at their disposal. MIAC’s MSR Hedge Advisory team relies on our internally developed CORE Model Suite. Accurate measurement of MSR price sensitivities is a complex and difficult challenge. Having the MSR Hedge Advisory, Model Development, and Software Development groups within a single firm facilitates a continuous feedback loop that simultaneously helps to improve both the hedge performance and the underlying models. In contrast, MSR Hedge Advisors that rely on externally developed vendor models can easily overlook model limitations or even implementation problems. Various model limitations are qualitative in nature and are difficult or even impossible to document.

It is worth repeating that MIAC GSA uses consistent attributes over the course of each calendar year to help market participants better quantify constant-quality MSR pricing changes and risk sensitivities arising from market conditions alone. This is displayed in Figure 1. Actual MSR portfolios will generally see an even larger shrinkage in duration and larger increase in price as their average note rates reset downward. However, there is an important asymmetry at play. Over periods when mortgage rates drop, the MSR universe changes rapidly as actual portfolios reset lower. This is what occurred during the 2019-2020 refinance wave. In contrast, when rates increase, the MSR universe changes slowly, and the difference between actual MSR portfolios and the GSA benchmarks will shrink. This means that changes in the GSA benchmarks will more closely approximate changes in MSR values reported on financial statements by public companies.

Figure 2: GSA Changes (Period-Over-Period) Source: MIAC Analytics™

MSR Analytics Updates

In Q3 2022, we updated our servicing cost assumptions to account for expected inflation in servicing costs. Although there are numerous measures of expected inflation, we strongly prefer market-implied measures which are both updated in real time and objective. We selected the 5-year break-even inflation rate published by the Federal Reserve Bank of St. Louis, which is based on the difference between the 5-year nominal CMT and the 5-year real TIPs rate. As of the date of implementation, that break-even inflation rate was 2.35. Although the impact of this change was small (under 2% of base case pricing), we will continue to monitor this implied inflation rate and implement changes as needed.

MSR Transaction Update

During the first half of 2022, MSRs were trading at levels not witnessed since before the Great Financial Crisis (GFC). Agency MSR sales of more than $2B that were mostly comprised of 2020 and 2021 vintage originations frequently transacted at multiples in excess of 5.25x. GNMA MSRs regularly traded at 4.0x and higher, with buyers sighting 20% home price appreciation in 2021 as support for waiving VA indemnifications. For competitive reasons, buyers routinely found ways to bid at or through their model estimates.

Fast forward to today and what was a sellers’ market quickly turned into a buyers’ market. While primary mortgage rates and float earnings rates are at a peak, the reason for the transition to lower execution prices can be blamed on a combination of buyer bandwidth, capital management, and/or budgetary constraints.

MSR liquidity, as evidenced by a banner year in transfers often at a premium execution level, has been nothing less than extraordinary. $523B in MSR transfers used to make for a strong year and that happened in just Q2 and Q3 of 2022. First quarter and sometimes second quarter auctions often produced interest from twenty or more buyers resulting in at least twelve bids on average. Early 2022 MSR acquisition success was cause for multiple bidders concluding that they don’t need any more product or at least product at a premium price, explaining why many buyers are now bidding at levels that are half to three-quarters of a multiple below their mark to model values. If offered today, the same portfolio may only attract four to six bids, often with elongated subservicing periods and transfers that are up to six months post sale date.

Speeds on 2020-2021 low coupon vintages are at or near their soft prepayment floor. Extension risk is the current hot topic of conversation. Mortgage market participants are actively debating the impact of mortgage assumptions within FHA/VA, a topic that has been dormant for the past 40 years. In fact, Ted Tozer, a leading figure in the mortgage industry and the past president of GNMA, has written an interesting article on the topic of expanding the use of mortgage assumptions to address the affordability problems in FHA. Tozer’s Urban Institute can be accessed here.

MSR execution levels for Agency MSRs should improve in Q1 2023 as more buyers work through their backlog of scheduled transfers and buyers receive their new 2023 acquisition budgets. However, GNMA MSR values are projected to remain soft as both buyers and sellers determine what, if any, capital restrictions might emerge as buyers slowly adapt to the new risk-based capital rules and potentially higher cost, should delinquencies rise in reaction to Fed intervention.

For more details regarding the timing of a typical bulk transaction, view the article, ‘What is an MSR?’, by Mike Carnes, available on MIAC’s website.

MIAC Perspectives: MSR Market Update – Q3 2022

Author

Mike Carnes, Managing Director, MSR Valuations Group

Mike.Carnes@miacanalytics.com

View MIAC Perspectives – Fall 2022 Issue