Macro Considerations

At a high level, considerations for how to choose 1) a pipeline hedge vendor and 2) the type of engagement with a hedge advisor, are dependent on characteristics of the lending institution, including:

-

Type of institution: i.e. independent mortgage banker, depository

-

Evolutionary stage of the firm: BE to Mandatory conversion? Becoming an agency direct seller? Shifting from portfolio lending to mortgage banking?

-

Staffing: availability/cost of experience/expertise in Pipeline risk management, mandatory delivery, TBA trading

These macro considerations help narrow the field of hedge advisors to be assessed. The answers to the three questions above will guide the firm to an appropriate place on the spectrum of engagement styles – with Full Service at one end, and Self Service at the other.

For example, an independent mortgage banker converting from Best Efforts to Mandatory with no experience in pipeline hedging would gravitate toward Full Service (at least to get started). In the case of most independent mortgage companies, the firm’s founding owners and majority partners are likely to have their roots in loan production, not in the secondary market or capital markets. Their expertise lies in making loans, not managing risk in the secondary market, which is a discipline unto its own.

By way of contrast, a regional bank selling directly to the GSE’s, retaining servicing, and looking to upgrade their risk management from a legacy spreadsheet approach, would lean toward a Self-Serve engagement, likely involving software licensing.

Alternatively, depositories (banks, credit unions), independent mortgage bankers typically have a narrower set of concerns and less demanding external counter-parties to satisfy, so the pool of acceptable hedge advisors is broader. A more complex regulatory environment guides depositories toward the top tier of vendors that meet more stringent compliance requirements, especially around model validation, disaster recovery, and data security (SOX, GLB, Dodd-Frank).

-

The upper echelon of hedge advisors is also characterized by true intellectual property embedded in the financial modeling that is the basis for licensable software. Because of the human element involved in risk management, there is as much art to pipeline hedging as there is science. The formal coding of these models into software doesn’t mean that the hedging results will automatically be better. However, in the right hands, better technology does enable a higher return on investment for the user.

-

Among the individual hedging vendors, the differences run from the structural to the technical. Several hedging vendors may be viewed as mono-line hedge advisors. They occupy one end of the spectrum of engagement, emphasizing high-touch, full-service hedge advisory services. This makes them popular with smaller and/or less sophisticated firms moving from Best Efforts to Mandatory.

Another set of hedging vendors occupies the self-service end of the spectrum, offering software for DIY’ers who don’t need or want any advisory component to the engagement. This makes them popular with large institutions that have robust staffing, experience, and resources to manage every aspect of the discipline.

A third set of hedge vendors is positioned to operate at both ends of the spectrum (and many points in between) providing a flexible engagement that enables the user to tailor the engagement to fit their evolving infrastructure.

Micro Considerations

Beyond these structural differences there are significant technical distinctions that further stratify the field of hedge vendors.

Within the field of pipeline risk management and hedge analytics, there’s an “Old School” and a “New School”.

The Old School methodology is characterized by any or all of the following:

-

Excel or Access database underpinnings

-

Pipeline MTM based on proxy pricing from the TBA market

-

Pipeline coverage weighted ONLY for Pull-Through

-

One-dimensional fallout analysis, and/or Pull-Through model

-

Definition of Flat means achieving a Zero Net Position

-

Absent or simplistic shock reports

-

Shock reports that demonstrate perfect symmetry between the Gain/Loss on the loans and Gain/Loss on the Hedges.

-

Sensitivity analytics that exclude duration and convexity of MSR component

The Old School methodology is also marked by the absence of a disciplined accounting for all of the risks to the embedded value of the pipeline. The Old School does not:

-

Measure “value at risk” from DAY 1 of the locked position via a client specific, daily loan-level best execution

-

Measure price/value sensitivity through an accurate and market-validated calculation of durations and convexity at the loan level and hedge instrument level

-

Measure and shock the MSR value or SRP component of the pipeline

Firms using the Old School method are at risk of being blind-sided, thinking they are covered appropriately, but are misled into believing that they were flat, or even long. In reality, they are short to begin with and become significantly shorter really fast in a big rally.

When the market eventually sells off, and it may do so violently, the Old School adherents and their clients, are likely to over-react by adding too much coverage in inappropriate coupons in an attempt to cover for an anticipated increase in pull-through. They will once again have their guard down, thinking they are covered properly, when in fact they are set up to get blind-sided again.

The absence of a dynamic risk model that integrates pull-through, durations, and MSR/SRP sensitivity is analogous to an NFL front line that is missing a Right and Left Tackle, leaving the quarterback exposed to a blind-side blitz.

The New School methodology has the blind side covered.

The New School perspective holds that adherents of the Old School are not measuring everything that they should, so their reports distort the reality of the client’s position. Old School analytics/reports may show that the client went into a particular market event with a flat (or even long) position, but if measured properly, they will typically be over-hedged by 10 to 20%. To make matters worse, the coupons they are hedged with are typically the most sensitive to changes in the market.

The “New School” of pipeline risk and hedge analytics addresses the blind spots inherent in the Old School approach. Here is how to cover the “Old School Blind Spots”:

-

Run daily loan-level best execution from Day 1 of the lock position based on the client’s specific risk profile and AOT contract terms

-

Perform loan-level sensitivity analysis on the MSR component in the loans and AOT contracts to accurately measure all pipeline and market risks

-

Calculate durations at the loan-level and hedge instrument level to calibrate the hedge on a duration weighted basis and hedge to the client’s actual execution

-

Deliver integrated best-execution and hedge analytics in one exercise to measure all exposures and optimize the position

Preparations

For most firms, migrating from a Best Efforts execution to a Mandatory execution represents an evolutionary step into a different business model. This entails a much deeper investment in the business, and often an organizational shift. The most significant shifts that occur in the transition from Best Efforts to Mandatory include:

-

Fallout Risk

-

Market Risk

-

Pricing/Basis Risk

-

Fair Value Accounting

-

Settlement Cash Flow

In order for the firm to succeed in the transition, and to achieve an attractive return on that investment, there are changes to the firm’s infrastructure that should be made, areas of expertise that probably need to be acquired, and new relationships that need to be established across the entire platform.

- IT and Systems Infrastructure: Some legacy systems supporting the firm in its Best Efforts days may be inadequate to efficiently support the additional complexity of the secondary marketing and risk management activities under mandatory execution.

- Pricing and Eligibility (PPE): At the outset of the transition to mandatory, firms will continue to use Best Efforts as the basis for their “street pricing” (that distributed to production units). As a result, most, if not all of the PPE’s in the market are adequate. Later in the firm’s evolution, they may consider shifting their pricing basis to mandatory (aggregator or agency) in order to get greater control over margins and provide a more stable price to the field. The firm will need a PPE that supports management of an upload from the firm for pricing distribution.

- LOS [Loan Originating System]: From the outset of the transition to mandatory, the firm will need to have an LOS that can be configured to capture and retain data relating to mandatory investor commitments, and purchase advice data in addition to the best efforts pricing for the loan.

This is necessary to facilitate the measurement of the additional gain-on-sale attributable to the mandatory execution. The LOS will also need to be configured to manage the “one-to-many” dynamics of investor commitments to allow for allocation of multiple loans to single investor commitment, as opposed to the “one-to-one” relationship in a Best Efforts execution. - Accounting/GL: Best Efforts commitments are technically considered a derivative hedging instrument. However, most independent mortgage banking firms don’t recognize this in their accounting methodology because each loan is mated to an individual investor commitment from the date of lock through investor settlement. Under mandatory execution involving the use of TBA MBS as the hedge instruments, their accounting systems need to be configured to support Fair Value accounting. This includes the separate recording of a month end Mark-To-Market on the parts of the position that are floating with the market (locked loans, uncommitted closed loans, and active hedge instruments), and these entries need to be made at the most granular level.

- Servicing: Currently, and for the foreseeable future, most firms who are transitioning into mandatory execution will defer (either voluntarily or involuntarily) to a transition into a servicing retention model for at least a year. If and when they do begin selling direct to the GSE’s, most will opt to outsource the servicing to a sub-servicer, at least until they have achieved significant scale. Some depositories may have legacy loan servicing systems that are engineered for a wide range of consumer loan servicing. These systems may suffice for a small scale effort, but will be challenged to efficiently service a mortgage servicing portfolio of a statistically relevant size.

- Organization/Culture: A common situation for independent mortgage bankers is for the culture of the firm to be singularly focused on loan production and have vested a great deal of control and power in the production units. That’s another way of saying that loan officers rule the roost and are used to getting their way. When the firm is in Best Efforts mode, the scope of a loan officer’s role tends to include activities that are (or should be) in the domain of secondary marketing: choosing investors for lock commitments, managing pricing extensions, renegotiations and re-locks. It’s also common for branches to be empowered to broker loans out to wholesale investors.The transition to mandatory requires a formal, disciplined, and centralized approach to all of these functions. Shifting those activities away from the production units and empowering the secondary marketing unit often requires some negotiation to make the production units feel that they are getting more than they are giving. Firms may offer to share some of the improvement in secondary market execution as the salvo, but they need to emphasize the need for the secondary marketing unit to control lock policies and procedures in order to mitigate the risks that could transfer to the firm under a mandatory execution.

- Mandatory Approval: The firm will need to approach its existing stable of investors and make a formal application for inclusion in their mandatory execution program. For the investor, this is likely a sad moment, as they stand to suffer a reduction in the margins they are making on the business they are buying from the firm. Typically, the approval should come within 30 days in the context of an existing relationship. In some cases, the investor will throw up a few road blocks to slow down the transition so they can continue to experience the wider margins for a little while longer. However, once the firm has made their intentions clear, the investor will have little choice but to approve the firm for mandatory execution if they want to continue to do business with the firm. For some firms, legacy performance issues with dormant investor relationships could preclude getting approved until those issues have been cleared through a negotiated settlement. These are highly situational, and the choice to settle in order to move forward will depend on the position of the investor in the market, the firm’s need for that investor’s execution, and how long it will take to recoup the firm’s “investment” in that relationship.

- Warehouse Financing: For some independent mortgage firms, legacy warehouse lenders may not support the mechanics of secondary marketing under a mandatory execution. Smaller mortgage bankers using local banking relationships to fund their pipelines may find that the relationship is not structured as a commercial line of credit. In these cases, the facility may be structured as “repo” where the warehouse lender actually takes possession of the loan at closing which disrupts the hedging, accounting, and mechanics of the mandatory execution. In these cases, the warehouse lender requires a “clear to close” from an investor before they will fund the loan. This works fine for a Best-Efforts execution where the firm is not authorized for delegated underwriting. However, the flexibility required for mandatory execution with delegated underwriting, means the firm will need to establish one or more relationships with other lenders whose warehouse facilities are properly structured. The terms of the financing will primarily be a function of the counterparty’s financials, profitability, liquidity, experience, reputation, and track record in the business. The firm will be required to meet certain covenants related to its financials (especially liquidity) in order to continue the relationship.

- External Auditors: It is common for firms to be engaged with external auditors who are in close geographic proximity, and are accounting generalists. Usually, these auditors have little or no experience with the nuances of Fair Value accounting that the firm will be faced with as it evolves into mandatory execution. This is often the case with firms who have evolved from broker to banker, or community and regional banks who are migrating from mortgage lending to mortgage banking. Usually, the firm will need to establish a relationship with an accounting firm that has developed expertise in Fair Value accounting, preferably for mortgage servicing rights as well as for the hedged pipeline. Currently there are several regional firms who are mono-line specialists in Fair Value accounting, as well national accounting firms that have units dedicated to this practice.

- Broker/Dealers: Firms who expect to hedge their mandatory positions using TBA Mortgage Backed Securities must establish relationships with SEC registered broker/dealers who can facilitate the efficient trading of these hedge instruments. Currently, there are several broker/dealers who specialize in this activity and who are focused on supporting independent mortgage bankers and smaller depositories with tangible net worth below $50 million. These “intermediary” broker/dealers cover their trading activity with the “primary” dealer community, which is comprised of large institutional broker/dealers with trading desks that may span many different fixed income securities beyond TBA MBS. The largest mortgage bankers and larger depositories can expect to be serviced directly by primary dealers, based on their counterparty strength and the amount of business they represent.The terms of the firm’s relationship with the broker/dealer will be a function of the firm’s financials, profitability, liquidity, experience, reputation, and track record in the business, and the firm will be required to meet certain covenants related to its financials (especially liquidity) in order to continue the relationship. There are several aspects of the hedging activity that can have an impact on the firm’s cash flow and cash position, and one feature of note in the broker/dealer relationship is a “margin call”. This feature obligates the firm to post cash to the broker/dealer when the mark-to-market value of the open TBA securities in the firm’s position declines beyond a certain point (the “threshold”, which may be different for each broker/dealer), where the position is “under-collateralized”. The cash is put on deposit for the benefit of the firm, and serves to reduce the amount owed by the firm to the broker/dealer at settlement across the entire position. Theoretically, the firm can ask for the cash back if and when the mark-to-market has rebounded to the point where the position is over-collateralized.Some broker/dealers require that the firm put cash on deposit up front, to provide a cushion against adverse mark-to-market movement. This is referred to as a “Margin Account”, and covers a certain amount of adverse market movement, beyond which, the firm is subject to a margin call, and must then post additional cash to maintain the collateralization of the position.

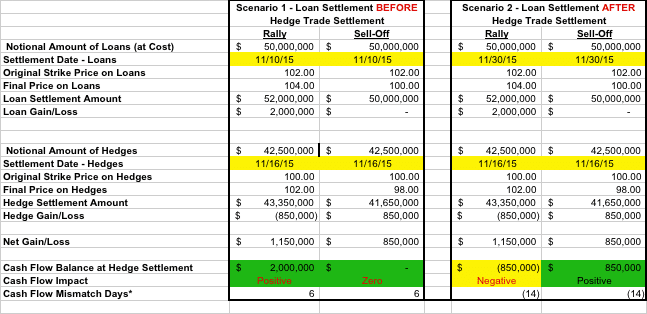

- Liquidity, Cash Flow: When executing via Best-Efforts, the firm’s cash management needs are based on a pretty simple one-to-one model where each loan is covered (“hedged”) by a commitment with the investor, and the recognition of gain-on-sale for each loan is immediate and absolute. The firm has execution certainty (as long as the data is static and the investor continues to operate), and their major cash outlay related to secondary marketing is the haircut on the warehouse line. The haircut is then recouped when the loan is settled with the investor and the funds are wired into the warehouse lender. If the loan doesn’t close (or the firm sells the loan elsewhere), the investor who provided the Best-Efforts commitment bears all the hedge costs.When the firm transitions to Mandatory execution, the loan and the hedge are de-coupled, and the cash-flow model changes. The firm has traded execution certainty for execution flexibility, and while the price an investor pays for the loan is still certain, the ultimate gain-on-sale for each loan becomes unknowable. There may be gains on loans that are offset by losses on hedge settlements, or the inverse may be true where losses on the sale of the loan are countered by gains on the settlement of the hedges. Since no single hedge instrument applies to any single loan, the locks taken on any given day, or any particular sub-group of loans, the ultimate performance of the firm is measured at the position level over a span of time, not at the loan level.Further complicating the situation is the fact that TBA MBS hedge instruments have specific settlement dates during the month, whereas loan settlements take place all month long. As a result, the firm may experience situations where gains from loan sales occur after payments of hedge settlements. This can result in a cash-flow mismatch as illustrated in the table below.

The firm can avoid the impact of these situations by engaging in AOT (Assignment of Trade) transactions with their loan investors. Essentially, the AOT shifts the hedge trade settlement obligation to the investor, and also provides an immediate credit to the firm’s broker/dealer account. This can also help the firm deal with a margin call scenario. However, not all investors are approved for AOT transactions with all broker/dealers, hence the need for a high level of liquidity for the firm at all times.

Simply put, Mandatory execution represents a very different and more sophisticated business model from Best-Efforts. Firms who plan to make the transition need to consider all the aspects identified above as part of their strategic plan for implementing a Mandatory execution strategy. They also need to choose the appropriate industry partners to support their efforts.