By Dean C. Hurley, Managing Director, Structured Products and Whole Loan Valuation Group

Dick Kazarian, Managing Director, Borrower Analytics Group

Markets Overview – The Environment

All of the major financial markets have suffered major disruptions as a result of the Coronavirus Disease 2019 (“Covid-19”). MIAC’s position is that only by properly modeling the expected future cash flows on these Level 3 assets, and then dealing with spreads independent of “panic bids”, can a correct ASC 820 valuation be reached. MIAC presents new Coronavirus 2020 Macrofactors scenarios, opinions, and observations about the markets in this issue.

Broad Markets Observations

- This is NOT 2008. The causes are different, financial institutions are generally better capitalized, prices have moved much faster, and the future recovery depends on different events.

- The recession is more likely to be “V” shaped than “U” shaped. How long it lasts and the damage to the economy depends on the effectiveness and length of government measures to stem new infection cases. We assume that three months is a likely situation.

- The downside is, like the 1918 Spanish Flu Pandemic, if government entities stem new cases with quarantine and social restrictions but lift restrictions too soon, the Coronavirus may show a resurgence, and re-imposition of restrictions will prolong the recession.

- Viable vaccines, treatments and “herd immunity” could happen soon (Hydroxychloroquine and Azithromycin are cited) or be more than a year away.

- Unemployment is likely to peak near 8-12% (see the record-breaking claims in Bureau of Labor Statistics, Unemployment Weekly Claims, March 26, 2020).

- Whole loan markets have essentially gone to bid only. Actual sales have halted as bidders have turned opportunistic (partly because they have difficulty gauging which loans have elevated default probabilities in the new environment), and the bids are often more than ten points back. Many bids are in the 40s to 50s, and sellers are not accepting.

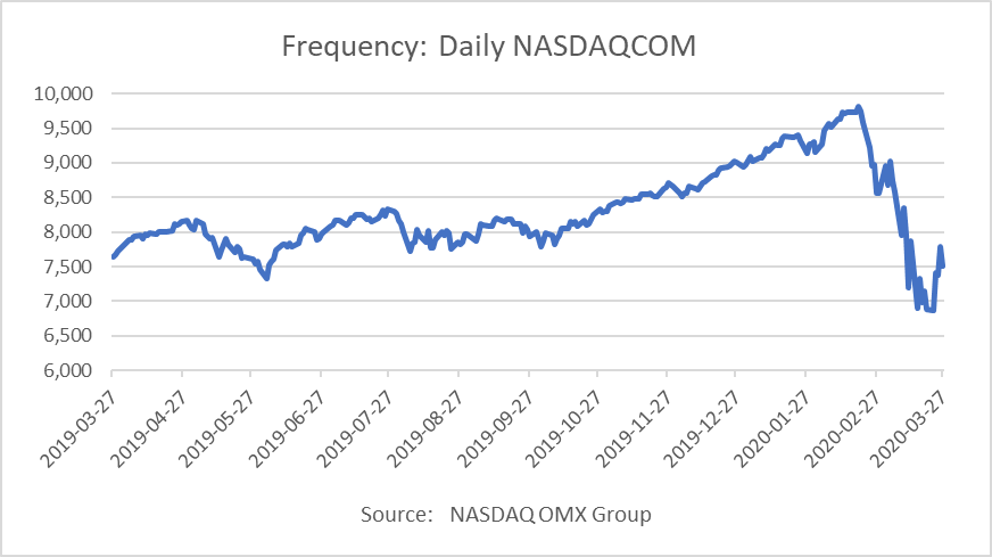

- Equities markets are on a rollercoaster ride, but now see a recovery with news of the $2tn government bailout. Additionally, Fed action to buy various financial assets has given equity markets a rebound.

Figure 1: Frequency: Daily NASDAQCOM Source: NASDAQ OMX Group

- REITs: Leverage is at an all-time low. Nevertheless, some Mortgage REITs were over-levered and have paid the price as of last week (March 24th). Those failing to meet margin calls include Invesco Mortgage Capital, MFA Financial, AG Mortgage Investment Trust and TPG RE Finance Trust.

Residential Housing Markets

- Housing Markets: With mortgage lenders offering forbearance and/or payment deferral, and many other lenders (including consumer unsecured lenders) doing the same, plus enhanced Federal stimulus benefits, we see default risks being substantially mitigated for at least 90 days and probably longer.

- With interest rates at record lows, there is a strong push for refinancing in the industry. Government programs are providing significant liquidity to the industry.

- However, home sales will be scaled back as potential buyers stay put during the lockdown phase which could last weeks or months.

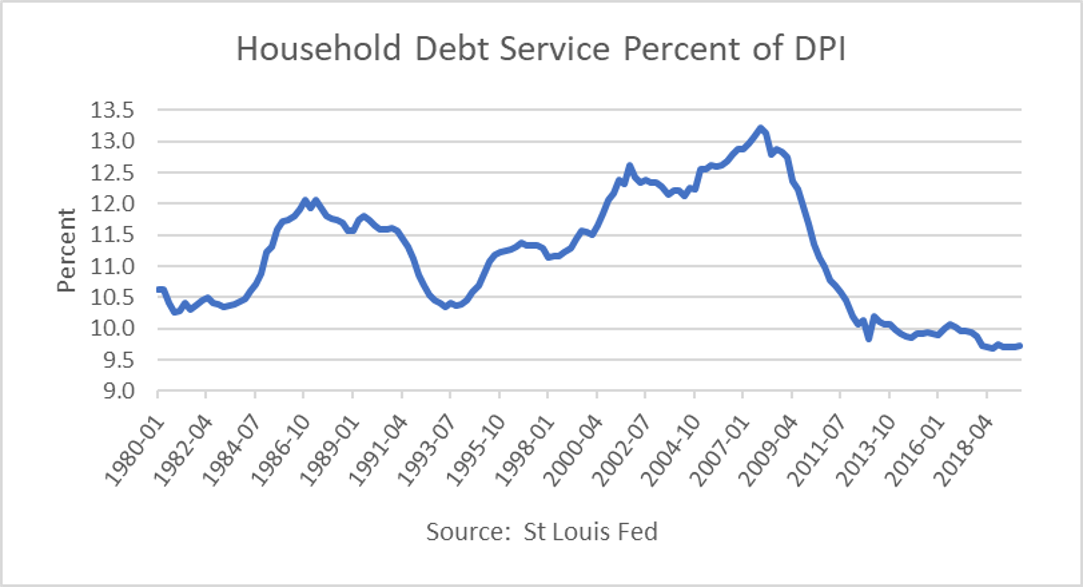

- Debt Service levels are at relative lows. This supports MIAC’s view that while housing will lose some value, a catastrophe is not in the offing.

- MIAC believes housing prices may decline somewhat in 2Q 2020 and will recover as restrictions are lifted and people start returning to work. Our scenarios conservatively show this.

Figure 2: Household Debt Service Percent of DPI Source: St. Louis Fed

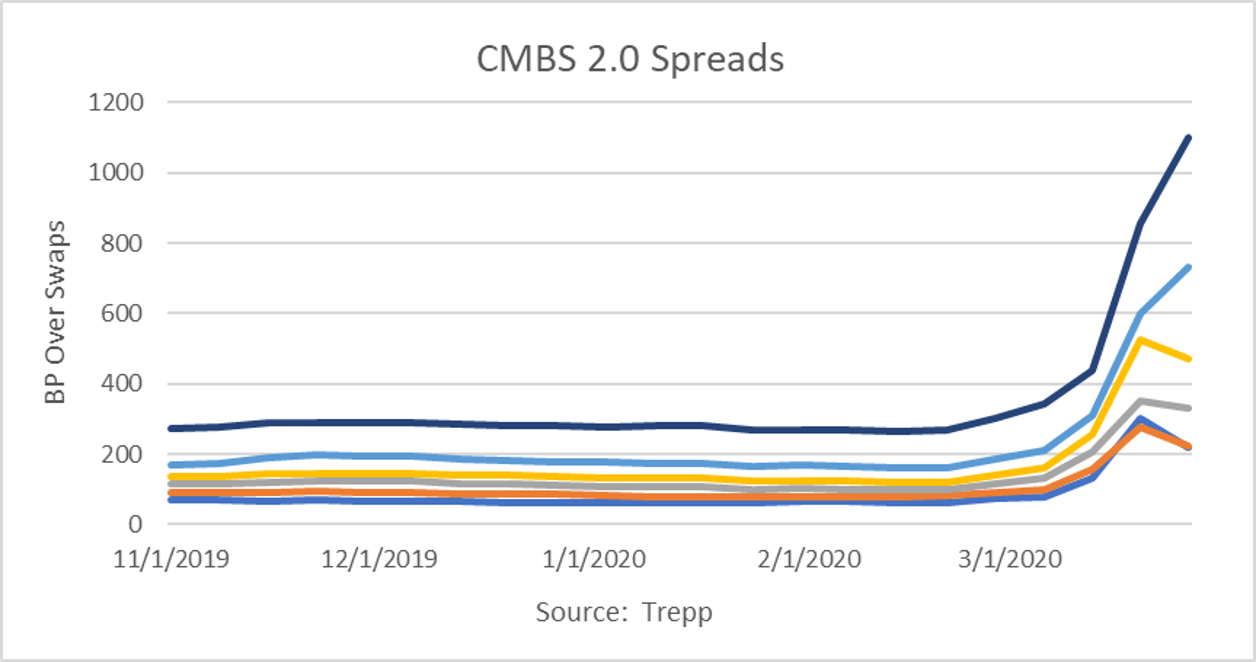

- CMBS 2.0: Spreads have risen dramatically. Live CMBS deal pricings like the $829 million conduit, CSAIL Commercial Mortgage Trust, 2020-C19, which priced March 11th, are the source of these numbers.

Figure 3: CMBS 2.0 Spreads Source: Trepp

Commercial Property Markets

- Retail was weak before the crisis and is getting hit hard due to closings. But many retail businesses have been able to remain open such as drug stores, supermarkets, take-out restaurants, and auto repair facilities.

- Lodging and Leisure industries were doing nicely but have been hard hit by travel bans and the sudden closing of their businesses.

- Office leasing is slowing, but in general, the sector is not immediately being hit as hard. Work from home will have a longer and more gradual impact on office markets. Because leases are longer-term, most tenants cannot immediately release space and are not as likely to default.

- Warehouse and Data Centers have a strong role in connecting the world and will continue to fare well in the new environment.

- Multifamily housing is more necessary than ever. Although exposed to unemployment risk, with enhanced unemployment insurance and government cash assistance extended through middle-income levels, multifamily housing is poised to do better than before.

- Self-Storage will remain largely unaffected or may see additional business, as some people take steps to pare back.

MIAC Coronavirus Macrofactor Scenarios

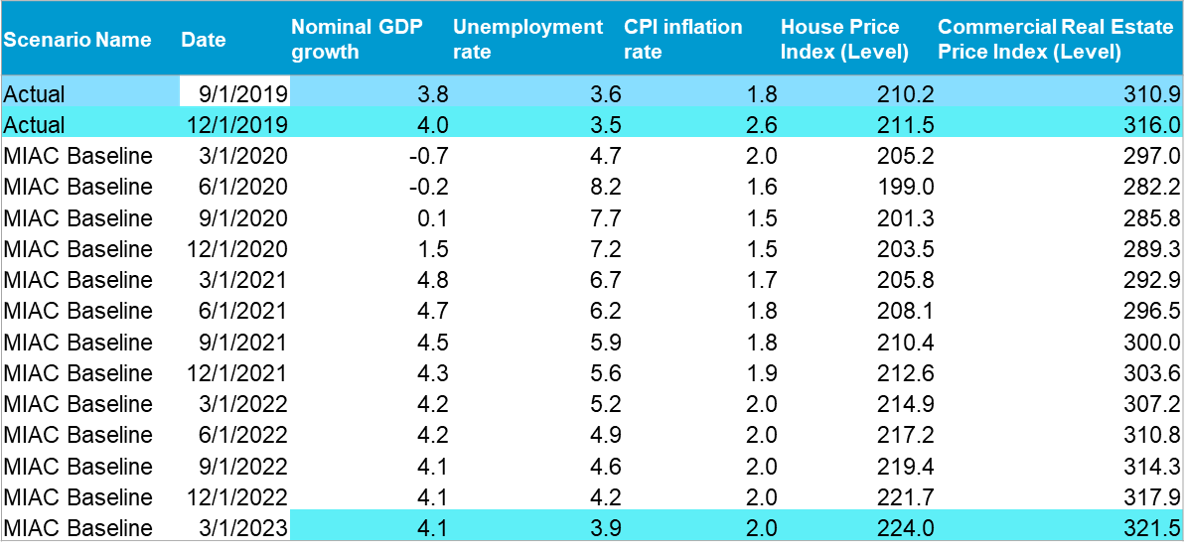

MIAC has created new macrofactor scenarios that show how we view the economy over the next three years, as a result of the Coronavirus pandemic. We have sketched out possible ranges of increased unemployment, lower Residential and Commercial property values, and reduced nominal GDP. Our Baseline scenario reflects the most probable outcome given current information. While no one can forecast future events with complete accuracy, MIAC believes that historical events, such as the 2008 housing crisis and several natural disasters, are helpful references when developing COVID-19 forecasts. Our updated forecasts are described in the following graphs and tables.

Figure 4: Fed Historical and MIAC 2020 Coronavirus Unemployment Scenarios Source: MIAC Analytics™

Figure 4: Fed Historical and MIAC 2020 Coronavirus Unemployment Scenarios Source: MIAC Analytics™

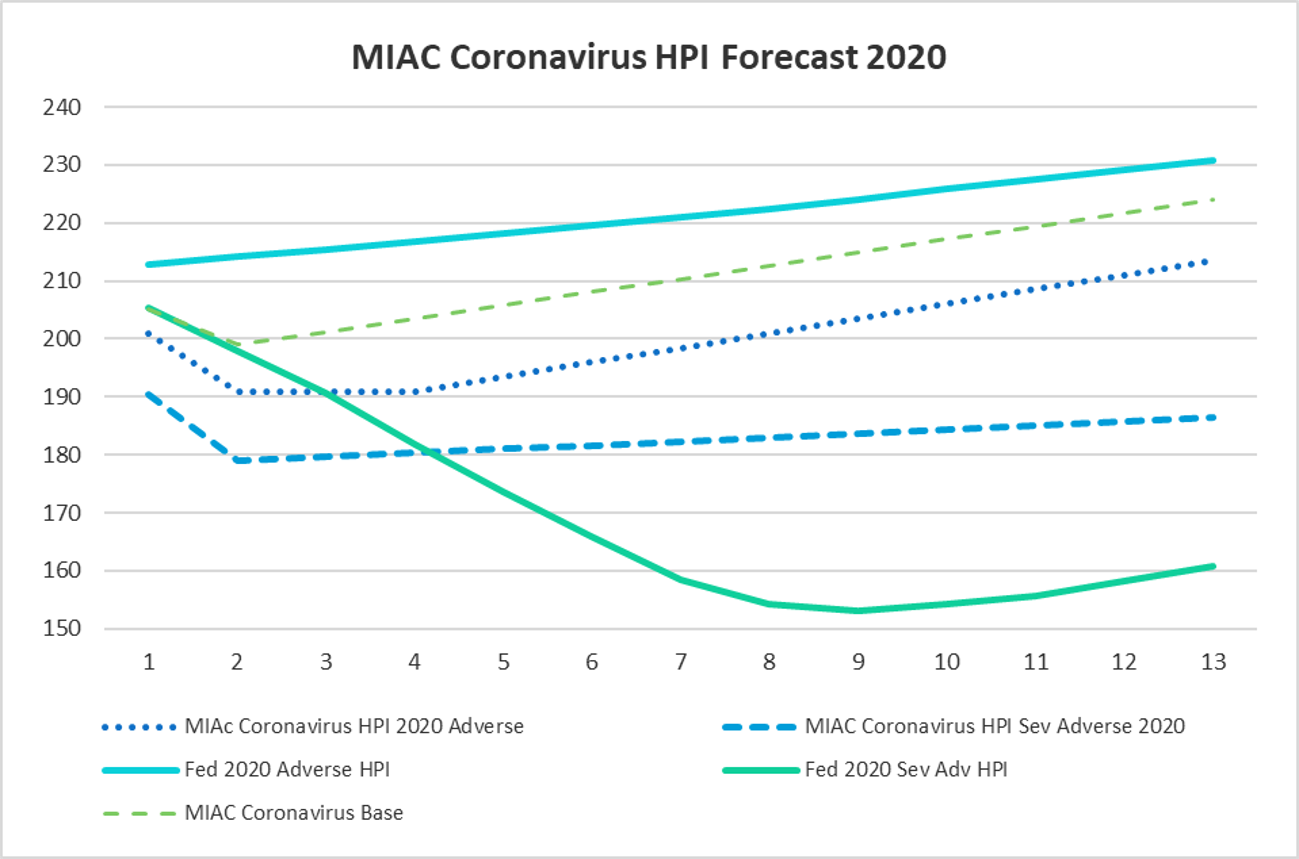

Figure 5: MIAC Coronavirus HPI Forecast 2020 Source: MIAC Analytics™

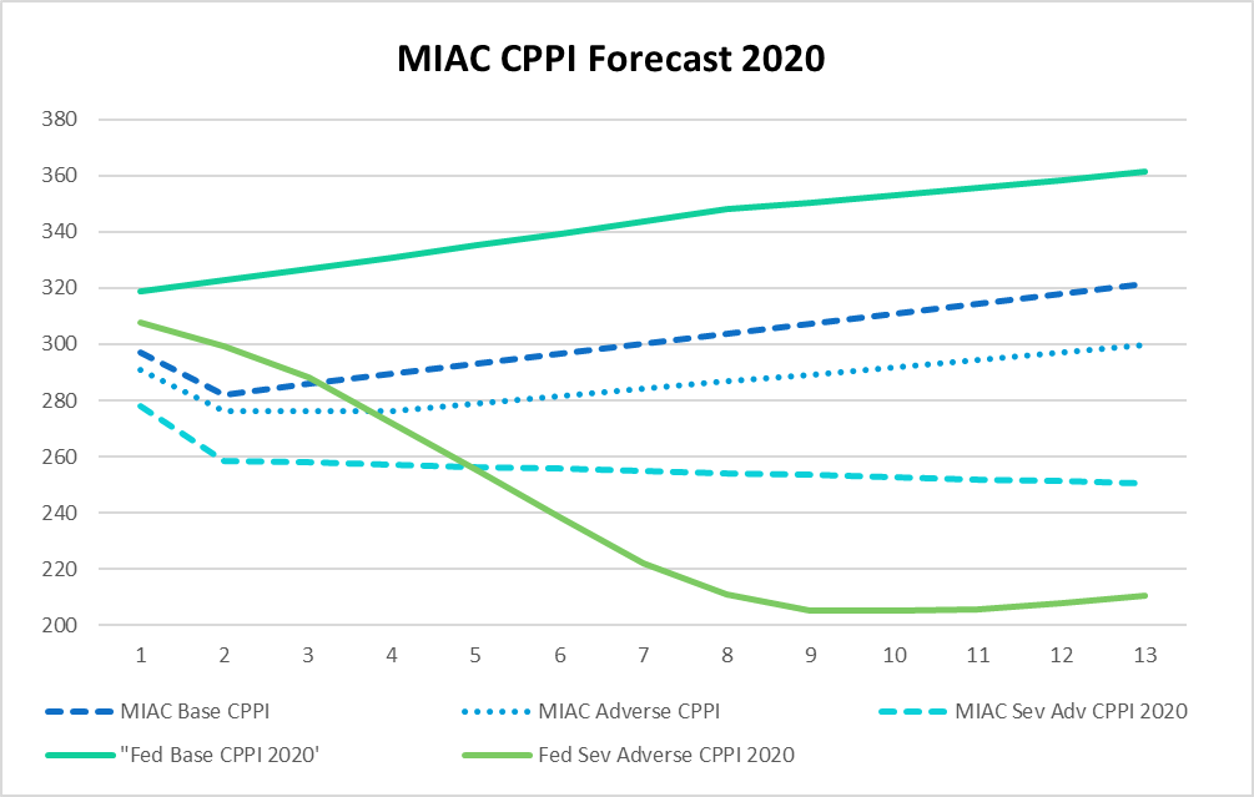

Figure 6: MIAC CPPI Forecast 2020 Source: MIAC Analytics™

How Did We Develop these Scenarios?

MIAC has reviewed data available to the industry through numerous sources. These include the Bureau of Labor Statistics, pricing data from JPM, BofA, Goldman and Trepp, commentaries from Rating Agencies, and forecasts of leading economists. We have also been reading extensively about the Coronavirus, the measures epidemiologists have been recommending, and the experience of past pandemics and disaster relief efforts, including loan modifications and the effectiveness of government efforts. Our review has informed our construction of these updated macrofactor scenarios.

Mark Zandi of Moody’s produced tables for the Brookings Institution showing the “at risk of job loss” employed population. The analysis shows that approximately 16.5% of jobs are at risk.

Figure 7: Zandi “COVID-19: A Fiscal Stimulus Plan” Source: Moody’s Analytics

MIAC feels that these levels of unemployment are unlikely to be reached. However, even with government mitigation efforts, there is no question that there will be serious disruptions with over three million new jobless claims filed last week, as compared to numbers in the 200 thousand in the weeks preceding.

Scenario Descriptions

- Base Case assumes only some people who are most at risk lose jobs, some federal mitigation of UER. Housing does not succumb much because of people that can hold on and delay plans, rather than panic sell (6% and then 5% quarter-over-quarter declines in HPI, followed by a faster growth resumption).

- MIAC feels that an 8.2% UER level will be the likely peak

- MIAC considers this outcome to be 80 – 85% likely

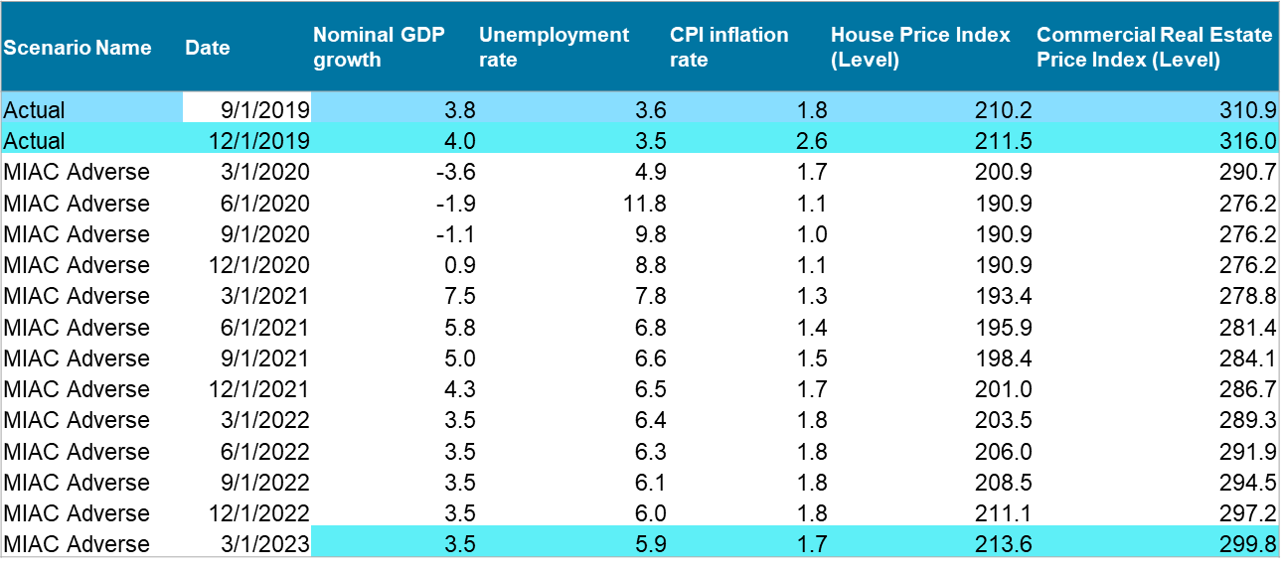

- Adverse Case assumes levels consistent with mainline forecasters at 11% UE peak and a delay in rehiring. Housing price declines are 8% and then 5% quarter-over-quarter, followed by a no-change period of two quarters.

- Other commentators, such as Goldman’s Jan Hatzius and Wells Fargo’s Jay Bryson, project job losses creating a UER above the 9% level

- MIAC considers this outcome to be only about 10 – 15% likely

- Severely Adverse Case – MIAC’s worst-case – assumes all these “at-risk industry” employees (plus some people working in jobs supporting these sectors) lose jobs. Housing price declines are 12% and 7% quarter-over-quarter, followed by very slow growth for four quarters.

- The peak UER in MIAC’s wort case is 16.2%

- We consider this outcome to be only 5% likely

MIAC Coronavirus Macrofactor Tables

Baseline Coronavirus Scenario

Adverse Coronavirus Scenario

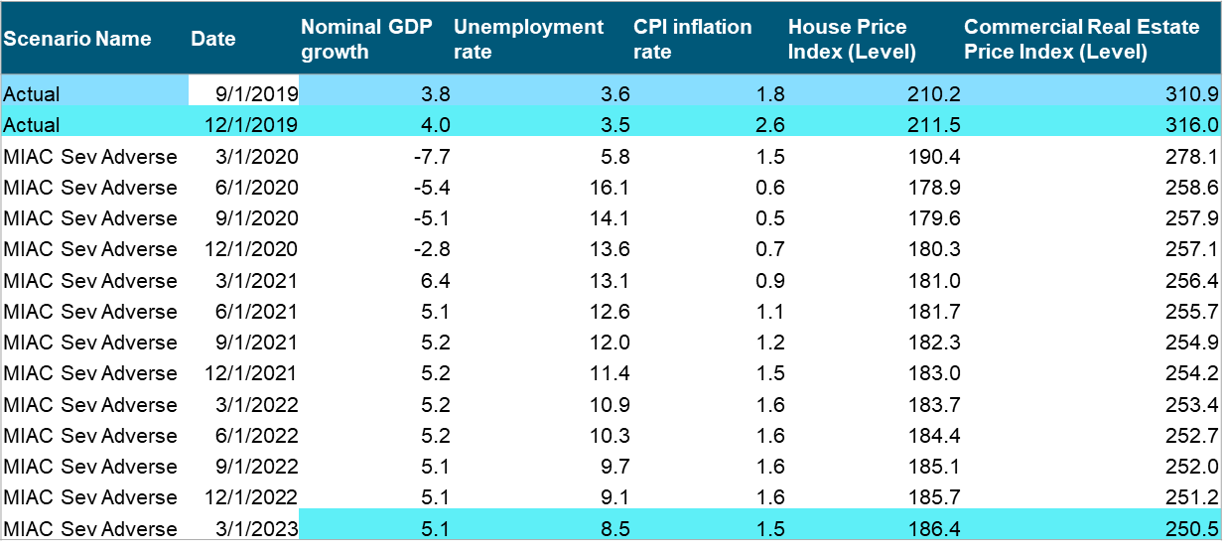

Severely Adverse Coronavirus Scenario

Valuation Using MIAC’s Vision and CORE Models

MIAC can see current market bid levels on whole loan assets, what ASC 820 classifies as Level 3. But these bid levels are not reflective of true market levels under ASC 820 Fair Value standards. Those hitting these bids are panic sellers, and the accounting profession has made clear that panic prices are not market prices.

- Lowball “panic” bids are made by opportunistic buyers who have the cash, and who feel that real levels of losses are likely to be far less than market participants assume now. This is what happened with RMBS and ABS bonds and whole loans from 2009 – 2010.

- All appraisals include a “market time” to realize the value started. Panic bids envision closing in very short timeframes (i.e., a week)

Market Spreads and Pandemics – True Market Spread Changes Reflect Uncertainty

Credit losses are always baked into panic-driven market spreads. To reach true market spreads, one must first determine the real level of losses likely to be realized because of the changes in the macro-environment.

- Then one can modestly adjust for uncertainty premiums to the pre-crisis spreads

- Our Vision 2.1 models (covering all loan types) and MIAC CORE 6.1 for Residential are all macrofactor sensitive, generating defaults, losses, and prepayments based on the macro factors in the forecast scenario

.

Research Insights: Modeling the Impact of COVID-19 on Whole Loans – Credit, Cash Flows and Valuation

Author

Dean C. Hurley, Structured Products and Whole Loan Valuation Group

Dean.Hurley@miacanalytics.com

Author

Dick Kazarian, Managing Director, Borrower Analytics Group

Dick.Kazarian@miacanalytics.com

View as PDF

Read this month’s MSR Market Update