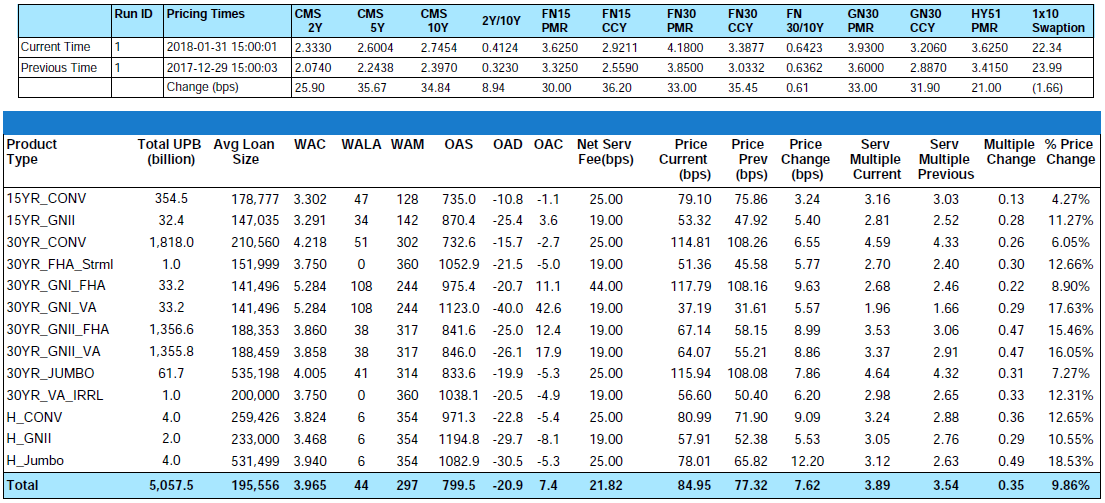

From 12/29/2017 to 1/31/2018, the MIAC GSAs™ Conv_30 Index increased by 6.05% and the GNII_FHA_30 index increased by a whopping 15.46%. In larger GSA cohorts, which are actively traded in the MSR market, the Conv30_3.0_2016 cohort increased by 4.15% and GNII_FHA30_3.0_2016 cohort increased by 9.61%. It has been years since any of us have had to worry about CPR floors. While CPR’s on FHA and VA product still have plenty of room to fall, we’re in the beginning stages of seeing CPR’s on Conv30 3.0% coupons leveling off. Consistent with our last monthly update, the price appreciation was attributable to more favorable economic conditions as well as tightening OAS spreads reflecting more aggressive investor appetite for MSRs. The Conv_30 Index OAS’s tightened 64 bps to 733 bps and GNII_FHA_30 Index OAS’s tightened 152 bps to 842 bps. The significant OAS tightening reflects a continued awakening of MSR bidders.

As measured by Bankrate®, month-over-month primary market 30-Yr conventional mortgage rates increased by a tremendous thirty-three (33) basis points to end the month of January at 4.18%. Quarter-over-quarter, 30-Yr conventional rates experienced a thirty-five (35) basis point increase. On its own, the back-up in rates was enough to appreciably increase MSR values but the favorable MSR market conditions were also felt in the form of higher benchmark earnings rates. From end-of-month December to end-of-month January, the 5-Yr swap rate, which is a common MSR market benchmark for earnings rates, increased by thirty-six (36) basis points to end the month at 2.60%. Likewise, quarter-over-quarter the fifty-two (52) basis point increase in the 5-Yr swap rate was in stark contrast to the quarterly change in the primary mortgage rate.

With such a persuasive forecast which is being partly driven by recent tax legislation, and as evidenced by MIAC’s GSAs™ (Generic Servicing Assets) the impact on MSR values have been nothing but positive. In 2017 nearly $540 billion in Fannie, Freddie, and Ginnie servicing rights changed hands. Most of the MSR transfers (over $406 billion) were bulk transactions which represent a 51.1 percent increase from 2016. Conversely, co-issue sales were down over 20% from levels achieved in 2016. The drop in co-issuance activity was partly due to an 11% decline in MBS issuance and partly due to the aggressive MSR prices being paid by the aggregators which in a “Best X” calculation sent product away from the co-issue buyers and into the hands of the aggregators.

Figure 1: Period-over-Period Price Change by Product Source: MIAC Analytics

Trading Volume

Lending further support to the above-referenced benchmarks, trading values witnessed on mostly larger pristine MSR offerings of Conventional 30-Yr product with note rates less than 4.00% trended in some instances above a 4.5 multiple and in extraordinary cases even hit a 5.0 multiple. To obtain the multiples referenced, numerous scenarios must exist. The seller must be a strong counterparty with significant net worth. The portfolio must provide significant economies of scale often categorized by $3 billion in unpaid principal balance or greater. The portfolio must have an attractive geography and an average loan size that is neither too high nor too low. Last but not least, buyers paying at the upper end of the referenced trading levels are in many instances applying forward biasing on modeled earnings rates.

Smaller conventional packages categorized as $500 million or less are seeing an uptick in trading volume as well but at prices that “on average” can be 5 to 15 basis points lower than the bid prices obtained on larger offerings.

Trading levels on mostly newer “at-market Ginnie Mae offerings”, comparatively speaking, continue to lag the conventional agency transactions and still range in the mid 3 multiple range. As with all transactions, Ginnie Mae execution levels are heavily influenced by service fee level, geography, deal size, borrower credit quality, counterparty, and to any potential exposure to Mother Nature, including hurricane and wildfires.

Figure 2: Conv 30-YR 3.50% 2018 GSA Index Source: MIAC Analytics

MIAC’s MSR Valuation department provides MSR valuation advisory services to over 200 institutions totaling nearly $2 trillion in residential and commercial MSR valuations every month. Learn about MIAC’s industry-leading valuation, brokerage, and/or GSA benchmarking, and please reach out to your MIAC representative for more information.

Mike Carnes, Managing Director, MSR Valuations, Capital Markets Group

Residential MSR Market Update – February 2018