Month-over-Month

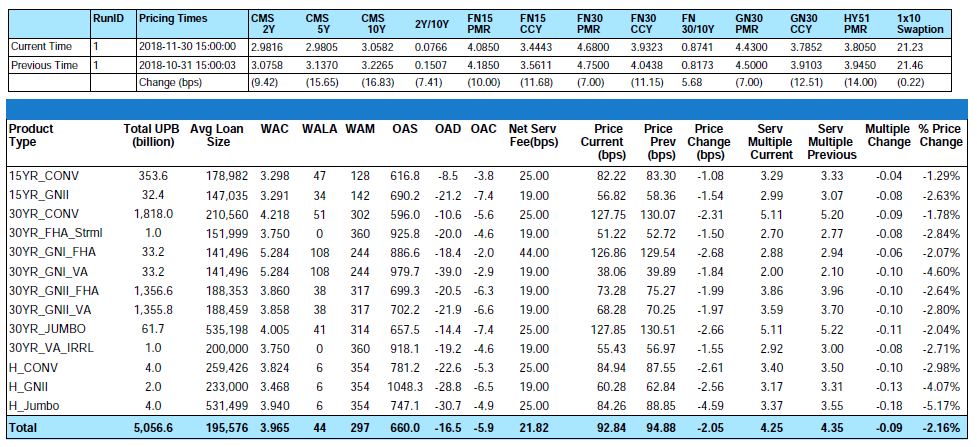

From end-of-month October to end-of-month November, the MIAC Generic Servicing Assets, (GSAs™) Conv_30 Index decreased by 1.78% and the GNII_FHA_30 index decreased by 2.64%.

In larger GSA cohorts, which are actively traded in the MSR market, the Conv30_3.5_2016 and GNII_FHA30_3.5_2016 cohorts respectively decreased by 1.98% and 2.65%. During the month of November, Conv_30 Index OAS’s widened to close the month at 596.0 bps for an increase of 20.7 bps. Likewise, GNII_FHA_30 Index OAS’s widened to 699.3 bps for a nominal month-over-month increase of 4.9 bps. Year-to-date Conv_30 Index OAS’s are tighter by a full 200 bps and GNII_FHA_30 Index OAS’s are tighter by an impressive 295 bps.

Figure 1: Month-over-Month Price Change by Product Source: MIAC Analytics

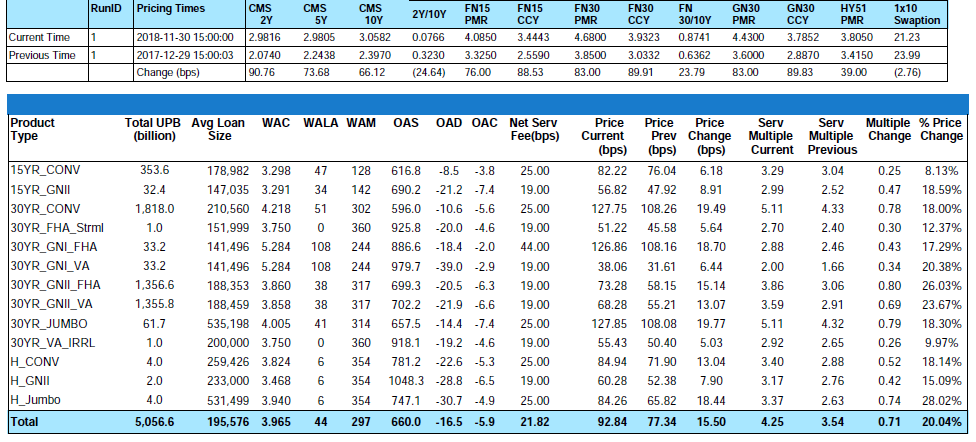

Figure 2: Year-to-Date Price Change by Product Source: MIAC Analytics

From end-of-month October to end-of-month November, primary rates as reported by Bankrate® decreased by seven (7) basis points. Year-to-date through end-of-month November, 30-Yr conventional primary rates are still higher by a full eighty-three (83) basis points. With just one month remaining in the year, the MBA end-of-year 30-Year Fixed Rate Mortgage Rate projection of 4.90% remained unchanged from their October forecast.

FDIC Proposes Basel III Relief for Certain Community Banks

In an effort to reduce the compliance burden imposed by Basel III, this month the FDIC voted to release a proposal that would simplify the capital treatment for an estimated 80% of community banks. Under the new FDIC proposal, institutions with less than $10 billion of assets and a more simplified tangible equity to total assets ratio of at least 9% may already be in compliance with Basel III capital requirements and therefore exempt from the more onerous Basel calculations. Banks with less than $10 billion in assets would be able to elect the community bank leverage ratio framework if they meet the 9% ratio and if they hold 25% or less of assets in off-balance sheet exposure, 5% or less in trading assets and liabilities, 25% or less in “mortgage servicing assets” and 25% or less in temporary deferred tax assets. The proposal makes available specifics about the computation of the community bank leverage ratio, the election process, and how the agencies intend on handling situations when banks’ leverage ratios worsen. The OCC and the Federal Reserve are expected to issue the proposal formally and comments will be due within 60 days of being published in the Federal Register.

In Ginnie Mae News

In our June ’18 addition, we discussed the role of non-banks and their continued ability to make advances during times of worsening economic strain. In late October, in an attempt to strengthen and safeguard the mortgage-backed securities market, Ginnie Mae issued their own concerns in a letter to some of the largest non-bank holders of Ginnie Mae servicing. While still loosely defined, Ginnie’s long term goal is clear — to lay the groundwork for mandatory stress testing that all Issuers/Servicers will eventually be obligated to adhere to. For those firms initially contacted, and all thanks to higher interest rates and rising borrower costs, the goal will be to develop a liquidity plan for right-sizing their operation in an environment where profits fall due to a combination of lower refinance volume and diminishing margins. Based on the non-bank presumption that they would not be subjected to CECL/CCAR-like stress testing, that will become mandatory for particularly larger banks, to some the letter came as somewhat of a surprise. While there will be more to follow on the matter, for those initially contacted, results will be due in 1Q’19.

Cash-out Refinance Volume

In an effort to meet profitability targets, issuers are increasingly targeting borrowers for their potential interest in pulling equity out of their homes. In the last 9 years, home values have risen sharply but worker pay has been expanding at a much slower pace causing homeowners to once again use their properties as ATM’s. Although the rate of cash-out refinancing is well below pre-crisis levels, according to Freddie Mac more than 80% of borrowers who refinanced their home in the third quarter chose the “cash out” option. This resulted in $14.6 billion in equity being extracted out of their homes which is the highest share of cash-out refinancing since 2007. For comparison purposes, in 2006 there were three continuous quarters where borrowers withdrew more than $80 billion.

MSR Transaction Activity

Recent “large” transactions which we define as deals containing $1 to $5 plus billion in unpaid principal balance have validated our very granular GSA prices. As for smaller offerings, the price/multiple spread is narrowing. Smaller offerings, defined as $500 million to $1 billion, are increasingly becoming the target of some larger buyers who have decided they’d rather not compete at the levels currently being offered for some of the largest offerings. Whether the transaction is large or small, one certainty is that most buyers are increasingly targeting pristine portfolios from well-capitalized sellers. While each buyer has their own definition of “thinly” capitalized or otherwise “at risk” counterparties, the sellers most apt to incur a price adjustment and/or fewer bids are those firms with a net worth less than $10 million.

The smallest packages categorized as $300 million or less in unpaid principal balance are trading at a robust pace too but at prices that “on average” range anywhere from 10 to 20 basis points lower than the bid prices obtained on larger offerings. In addition to the reduced economies of scale afforded by larger MSR trades, acquisition costs is one of the reasons that smaller deals can trade at a discount to larger offerings. The legal and due diligence costs that a buyer may incur to acquire a portfolio can influence how a firm might bid on a smaller trade. Even so, it is the smaller trades that can often create the largest margins and in a quest for margin, increasingly we see larger buyers bidding on smaller offerings but sometimes with a more rigid approach to price and term negotiations.

Regardless of size, not all bids are as they might appear on the surface. Differences in prepay protection periods, non-reimbursable advances, non-payment for assets that are 60 or more days delinquent, fee deducts for seriously delinquent MSRs, loan kicks, and possible set-up fees are just a few of the pitfalls that can quickly affect a seller’s net execution price.

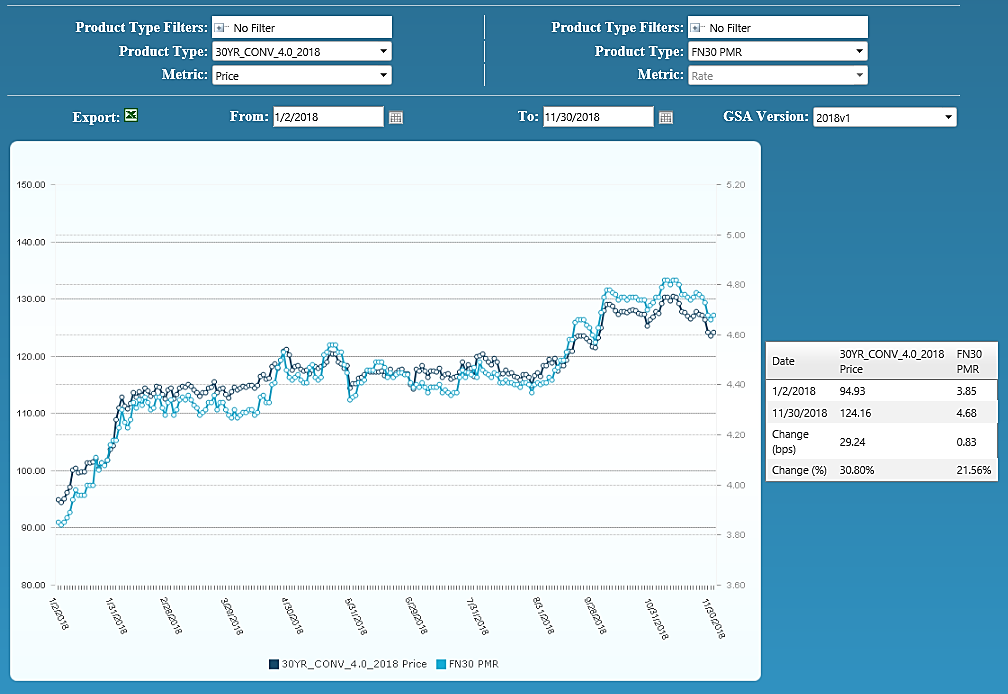

Figure 3: Year-to-Date Conv 30-YR 4.00% 2018 GSA Index Source: MIAC Analytics

MIAC’s MSR Valuation department provides MSR valuation advisory services to over 200 institutions totaling nearly $2 trillion in residential and commercial MSR valuations every month.

Residential MSR Market Update – November 2018

Author

Mike Carnes, Managing Director, MSR Valuations, Capital Markets Group

Mike.Carnes@miacanalytics.com